Source: Statista

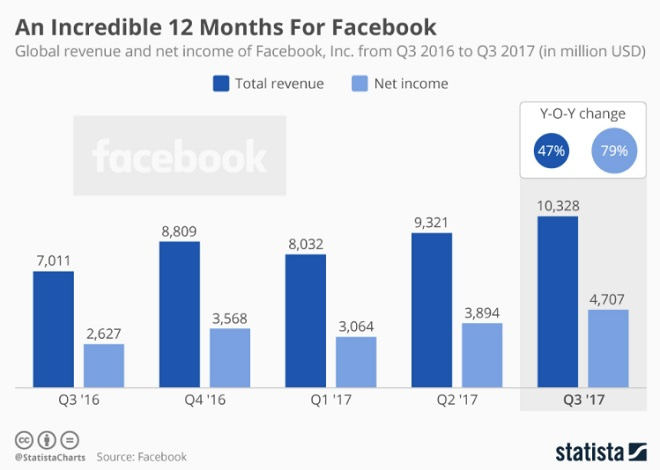

Facebook has again flown past expectations in its latest quarterly earnings report. As our infographic shows, in Q3, the company posted a year-on-year increase in net income of 79 percent. Moving up from the $2.6 billion in 2016, the last three months put $4.7 billion in Facebook’s coffers. Revenue is a similar story, with a 47 percent year-on-year increase to $10.3 billion.

Investors have nevertheless been spooked though, driving share prices down by as much as 2 percent in response to Zuckerberg’s warning that operating expenses in 2018 will rise by up to 60 percent. Citing the need to protect the company’s services from the kind of misuse seen during the 2016 U.S. presidential election, he said the company is “serious about preventing abuse on our platforms. We’re investing so much in security that it will impact our profitability. Protecting our community is more important than maximizing our profits.”

Like this:

Like Loading...