When Covid-19 hit the United States with full force in early 2020, thousands of businesses were forced to shut down, millions of Americans lost their jobs within weeks and, as a result, U.S. gross domestic product plummeted by an unprecedented 28 percent in Q2 2020. At the time, there was a lot of uncertainty over how quickly the economy would bounce back, but now, almost four years later, it can safely be said that the recovery has been nothing short of impressive.

After total nonfarm employment returned to its pre-pandemic level in June 2022, the labor market has remained remarkably strong until now, despite the Fed’s best efforts to cool it down to tame inflation. More importantly though, the economy as a whole has also returned to its pre-pandemic growth trajectory, as consumer spending has proven surprisingly robust throughout the post-Covid recovery and the ensuing inflation crisis. According to the second estimate of Q4 and full-year 2023 GDP released by the U.S. Bureau of Economic Analysis (BEA) on Wednesday, real GDP grew 2.5 percent in 2023, re-accelerating from 1.9 percent in 2022 despite the Fed’s restrictive policy stance.

As the following chart illustrates, Covid-19 did put a dent in U.S. economic growth but, thanks at least in part to generous stimulus spending in the early phase of the pandemic, it didn’t throw it off its trajectory permanently. Measured in chained 2017 dollars, U.S. GDP amounted to $22.37 trillion in 2023, up 8.1 percent from 2019, the last year unaffected by the pandemic. That equates to an average real GDP growth rate of 2.0 percent over the past four years, which is quite remarkable considering the global circumstances under which this growth was achieved.

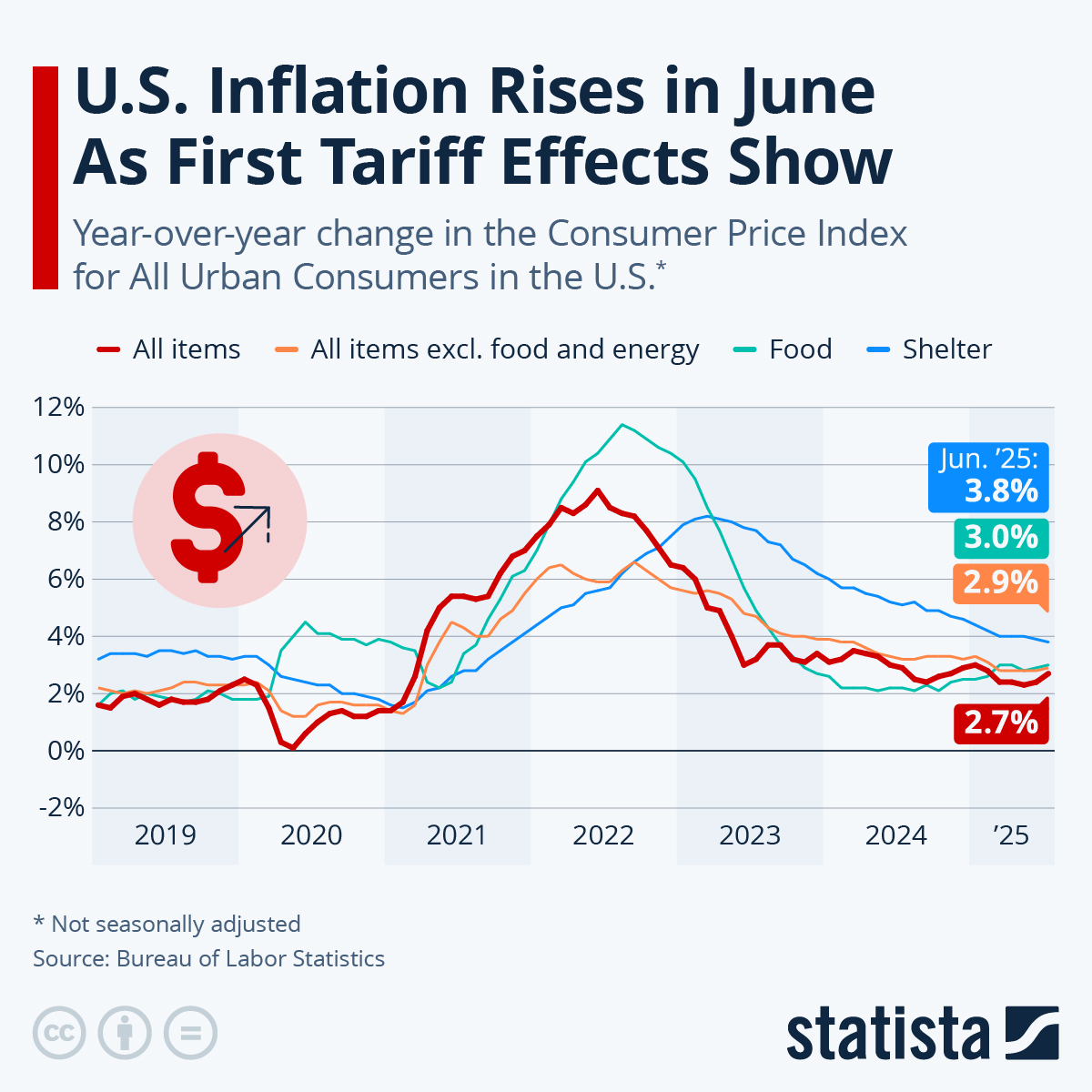

Inflation in the U.S. continued its downward trend in June, falling to the lowest level in more than two years, as the Consumer Price Index for All Urban Consumers (CPI-U) increased by 3.0 percent compared to the same month a year ago. That’s the smallest increase since March 2021, when inflation was just beginning to heat up.

Back then in the spring of 2021, the high inflation readings could largely be explained by the so-called base effect, as prices had fallen sharply at the onset of the pandemic a year earlier, when demand for many goods and services had suddenly dried up. Due to that initial dip in consumer prices, year-over-year comparisons were exaggerated for a while, but towards the end of 2021 inflation became a real concern, which turned into a global crisis when Russia attacked Ukraine, resulting in surging food and energy prices.

The fact that the war in Ukraine has been dragging on for more than a year now is also the reason why the latest, pleasantly low inflation readings should be taken with a pinch of salt. Following Russia’s invasion of Ukraine in late February of 2022, consumer prices, especially for food and energy, climbed sharply, meaning that current price levels are compared to a period of already elevated prices. In fact, energy prices dropped 16.7 percent over the last 12 months, meaning that the overall reading would have been higher without their cooling effect.

The core CPI excluding food and energy increased 4.8 percent – the lowest rate since October 2021 – while the index excluding just energy increased by 5 percent year-over-year. By far the largest driver of inflation in June was the cost of shelter. With rents and owners’ equivalent rents of residences increasing 8.3 and 7.8 percent in June, respectively, the index for shelter accounted for more than 70 percent of the all-items increase.

Lack of Listings and Increasing Supply Constraints Continue to Limit Existing and New Home Sales

Washington D.C., May 19, 2021 (PRNewswire) – Expectations for full-year 2021 economic growth were revised upward in May to 7.0 percent, a modest improvement from last month’s projection of 6.8 percent, attributable primarily to stronger-than-expected first quarter real GDP growth and an improved near-term outlook for consumer spending, according to the May 2021 commentary from the Fannie Mae (OTCQB: FNMA) Economic and Strategic Research (ESR) Group.

The additional strength in consumer spending was previously projected to occur later in 2021 or early 2022, but recent incoming data increasingly points to eagerness on the part of consumers amid continued progress mobilizing COVID-19 vaccinations and waning virus-related restrictions. With stronger growth expected in the current year, the ESR Group slightly downgraded its expectations for 2022 real GDP growth by 0.2 percentage points to 2.8 percent. Despite expectations that the economy will continue to grow over the forecast horizon, downside risks to the forecast are increasing and include supply chain disruptions, labor scarcity, and rising inflationary pressure.

On housing, the ESR Group expects home sales in 2021 to increase 6.3 percent as the industry continues to grapple with strong demand and limited supply. While a lack of existing homes for sale is heightening the demand for new homes, supply constraints – most notably lumber – and a dearth of buildable lots, as well as hiring difficulties, are limiting homebuilders’ pace of single-family construction, which is still forecast to be 24.8 percent higher in 2021 than 2020. The ESR Group’s mortgage origination forecast remains largely unchanged at $4.1 trillion in 2021, but the recently lower mortgage rate environment contributed to a slight shift in its composition, with the expected refinance share ticking up a couple percentage points to 55 percent.

“While most indictors point toward brisk economic growth over the second quarter, the combination of a disappointing employment report and an unexpectedly strong burst of inflation has raised in the minds of many market participants the potential confluence of broad-based supply restraints, very strong house price growth, and the posture of monetary and fiscal policies,” said Doug Duncan, Fannie Mae Senior Vice President and Chief Economist. “Supply constraints across multiple sectors are pointing toward ongoing price pressure, most prominently in microchips and the auto sector. This has yet to significantly affect mortgage rates, except to the extent that the rise in the 10-year Treasury since the beginning of the year contains an increased expected inflation component and has prevented mortgage rates from retreating further from their temporary recent peak.”

Duncan continued: “Stronger inflation and a resultant move in interest rates are risks that we believe should be monitored. As the effects of expansionary monetary policy continue to work their way through the economy, inflationary expectations may continue to rise. This could lead to prices rising further even with growth concurrently slowing in the presence of diminished labor market slack and waning fiscal policy support. If such a scenario were to play out, the question then becomes whether this necessitates a response by the Federal Reserve. While momentum in the housing market will likely continue in the near term, this is an increasingly important consideration for 2022.”

About Fannie Mae Fannie Mae helps make the 30-year fixed-rate mortgage and affordable rental housing possible for millions of people in America. We partner with lenders to create housing opportunities for families across the country. We are driving positive changes in housing finance to make the home buying process easier, while reducing costs and risk. To learn more, visit: fanniemae.com | Twitter | Facebook | LinkedIn | Instagram | YouTube | Blog