Source: car.org

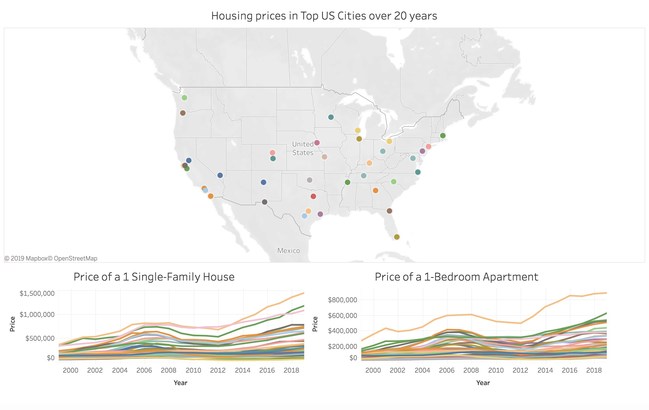

A new study published by PropertyClub shows that homeownership is getting more expensive nationwide, with real estate prices in most major US cities surpassing those seen during the 2007-2008 housing bubble.

New York, NY – April 4, 2019 (PRNewswire) The American dream of homeownership is becoming more expensive than ever according to a new study published by

PropertyClub’s study found that cities on the west coast have quickly become more expensive than ever, with the San Francisco and Los Angeles metro areas leading the charge. Between 1999 and 2019, single-family homes in San Francisco and Los Angeles have seen price increases of 304 percent and 275 percent respectively while single-family homes in Oakland have seen an increase of 337 percent. Other major cities to see significant price increases in the segment include New York City, with a 225 percent increase, and Washington DC, which with a 412 percent increase has seen the highest jump nationwide.

When it comes to affordability, cities like Wichita, Oklahoma City, and Cleveland received high marks, with Cleveland being the only city where single-family home prices are lower today than they were 20 years ago. It would only take approximately three years of savings to purchase a single-family home in Cleveland or a one bedroom apartment in Wichita.

About PropertyClub

PropertyClub, Inc. is New York City’s premier blockchain-powered real estate marketplace and your number one source for NYC real estate. Users can earn cash and crypto rewards when they rent or buy their next home including buyer rebates of up to 2 percent of the purchase price.

Press Contact: Andrew Weinberger, andrew@propertyclub.io

Related Images

propertyclubs-20-year-analysis-of.png

PropertyClub’s 20 Year Analysis of Real Estate Prices in 50 Largest US Cities (1999-2019)

cities-with-the-highest-real.png

Cities with the Highest Real Estate Price Increases 1999-2019

cities-with-the-lowest-real-estate.png

Cities with the Lowest Real Estate Price Increases 1999-2019

– A new survey from Clever Real Estate reveals a full profile of the Millennial home buyer, uncovering insights from how they find homes to what they want to buy. Key insights include:

– Millennials are thinking long term about where they buy: They value safe neighborhoods and good school districts over walkability and short commutes.

– Millennials are 52% more likely to buy a multi-family property compared to older generations (Generation X and Baby Boomers).

– Millennials won’t shy away from a fixer-upper. 67% would put an offer on a home that needs major repairs.

St. Louis – Jan. 17, 2019 (PRNewswire) The 2019 Clever Real Estate Home Buyer Report surveyed 1,000 U.S. residents in the market to buy a home within the year. Over half of respondents were classified as Millennials.

![]()

78% of Millennials are first-time home buyers and 38% aren’t working with an agent to find a home (and might not realize sellers usually pay buyer agent commission).

Despite the popular belief that Millennials are short-sighted and flippant, most Millennials value good school districts and safe neighborhoods over walkability and short commutes. Only 9% of Millennial home buyers are afraid of being tied down to a home. Millennials believe buying a home is a good investment, and they’re thinking long term about their decisions.

In fact, Millennials are looking to get into real estate investing. Millennials are 52% more likely to buy a multi-family home than older generations. They see the benefit of becoming landlords and generating passive income to help pay off their debt.

With Millennials struggling to pay off debt and save for a down payment, many home shoppers realize they can’t afford a huge mortgage payment every month. Due to their financial constraints, Millennials are also willing to take on properties that need repairs. 67% would put an offer on a home that requires major repairs (this could be dangerous for many buyers that don’t realize the true cost of homeownership).

The full report, including insights, analysis, raw data and methodology, can be found here:

https://listwithclever.com/real-estate-blog/millennial-home-buyer-report/

Clever Real Estate

Clever Real Estate connects top real estate agents with home buyers and sellers at a discount rate. This survey was conducted using Pollfish to help Clever better understand the Millennial home buyer.