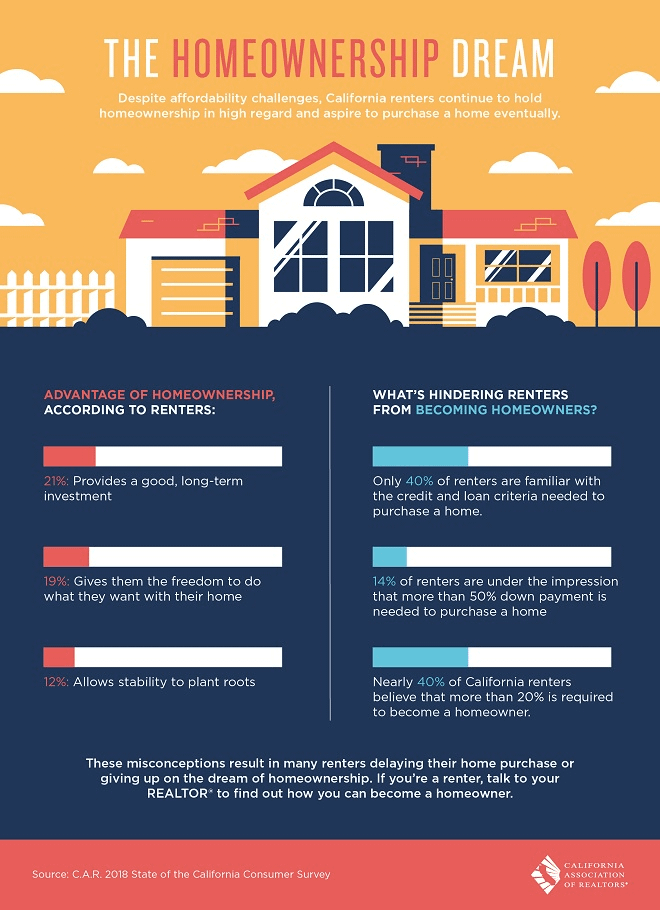

Washington, D.C. – January 14, 2019 (nar.realtor) Homeowners and non-homeowners both strongly consider homeownership part of the American Dream.

![]()

That is according to new consumer survey data from the National Association of Realtors®, which revealed that among those polled, approximately 75 percent of non-homeowners believe homeownership is part of their American Dream, while nine in 10 current homeowners said the same.

NAR’s Aspiring Home Buyers Profile analyzed 2018 quarterly consumer insights from its Housing Opportunities and Market Experience (HOME) survey(1) to capture the housing expectations and sentiments of non-homeowners – both renters and those living with a family member.

When non-homeowners were asked for the chief reason why they currently do not own a home, most respondents said it was because they were currently unable to afford a mortgage. Over the last quarter of 2018, 43 percent of non-owners said they did not own a home because they were not in a position to purchase, which was down from the third quarter of 2018, when 49 percent of non-homeowners answered the same. Also in the 4th quarter, 33 percent of non-homeowners said they do not own because current life circumstances are not suitable for ownership, while 16 percent said they need the flexibility of renting.

In addition, the survey looked at the main reason why non-homeowners would buy a home in the future. Throughout 2018, 28 to 31 percent of non-owners each quarter said an improvement in their financial situation would be the top reason that would encourage them to buy a home in the future. In each quarter, 26 to 30 percent of non-owners said a change in lifestyle – such as getting married, starting a family or retiring – would be the primary reason they would make a future home purchase.

Lawrence Yun

For this year’s survey, homeowners and non-owners were also asked about adult family or friends moving into their homes, the span of time this individual(s) lived within the household, and if they thought about moving to a new home because of the change.

According to the survey, 11 percent of homeowners had an adult child move into their residence, while 5 percent of non-owners had an adult move into their home.

Of those who had someone move into their home, 44 percent said that the individual intended to live with them for over one year or to stay permanently. Forty-four percent of non-owners reported that the individual planned on living with them for between six months to one year.

Eighty-eight percent of those surveyed who had someone move into their home reported that their living situation remained acceptable and therefore did not warrant consideration of moving into a different home. Twelve percent said they did consider moving or ultimately did move due to their home situation changing.

“While home sales were slightly down in 2018, there is still a sizable pent-up housing demand. Economic growth, interest rates, and the supply of moderately priced-homes will dictate how well the real estate industry will do this year,” said Yun.”

About NAR’s HOME survey

In each quarter of 2018, a sample of U.S. households was surveyed via random-digit dial, including half via cell phones and the other half via landlines. The survey was conducted by established survey research firm, TechnoMetrica Market Intelligence. A total of 8,140 household responses are represented.

The National Association of Realtors® is America’s largest trade association, representing more than 1.3 million members involved in all aspects of the residential and commercial real estate industries.

# # #

1. NAR’s Housing Opportunities and Market Experience (HOME) survey tracks topical real estate trends, including current renters and homeowners’ views and aspirations regarding homeownership, whether or not it’s a good time to buy or sell a home, and expectations and experiences in the mortgage market. HOME survey data is collected on a monthly basis and is reported each quarter. New questions are added to the survey each quarter to reflect timely topics impacting real estate.

Media Contact:

Quintin Simmons

(202) 383-1178

Email