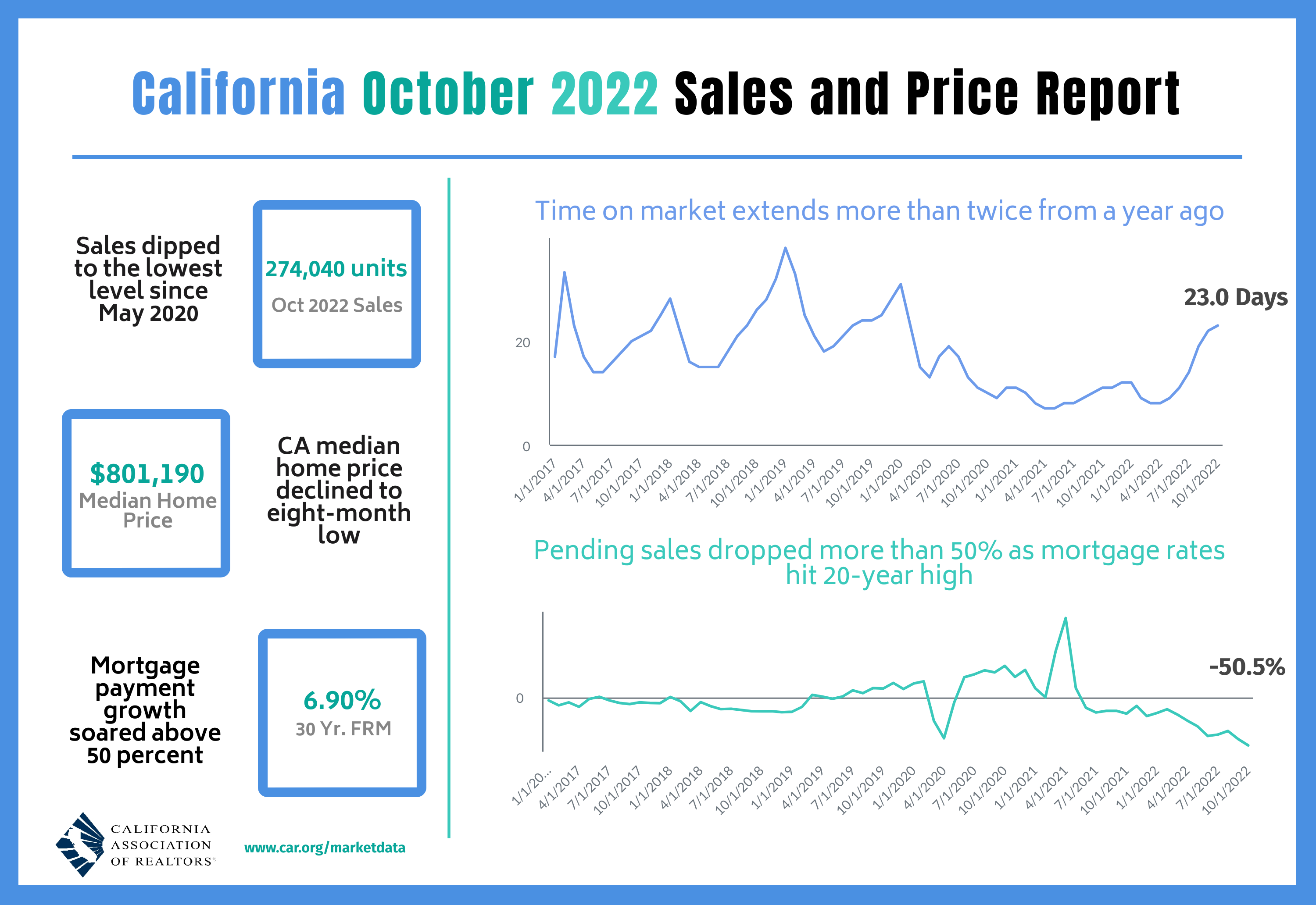

Source: car.org

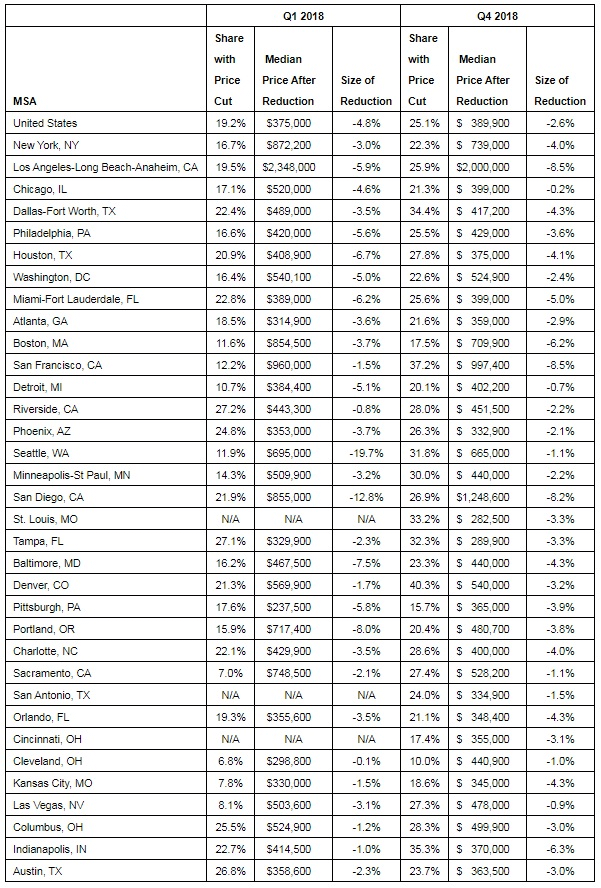

– Nearly all of the nation’s largest housing markets saw the share of new construction homes with price cuts increase between the beginning and end of 2018

– About a quarter of all new construction homes saw a price cut in the fourth quarter of 2018, with the typical drop throughout the quarter being 2.6 percent.

– The median list price after a price reduction was $389,900 at the end of the year.

– The biggest price reductions at the end of the year were in San Francisco and Los Angeles, where new construction homes are among the most expensive in the country.

Seattle, WA – Jan. 17, 2019 (PRNewswire) Home shoppers may be able to find a better deal on a new construction home than they could a year ago. A new Zillow® analysis finds that price cuts were more common in the fourth quarter of 2018 than in the first quarter.

![]()

Across the country, 25.1 percent of new construction homes had a price cut in the fourth quarter, compared with 19.2 percent of new homes in the first quarter of the year. This mirrors a trend seen in the overall housing market, with price cuts becoming more common.

Eleven percent of buyers last year bought a new construction home, according to the 2018 Zillow Group Consumer Housing Trends Report. For many of them, everything being new was a top reason for buying a new construction home instead of an existing home. More than a third of new construction buyers also felt it represented the best value for their money – and they might be getting even more value now.

Buyers were most likely to find a price reduction in Denver, where 40.3 percent of new construction homes had a price cut in the fourth quarter of the year. At the beginning of the year, just 21.3 percent of newly built homes had a price cut. In Austin, price cuts were less frequent at the end of the year than they were at the beginning.

New homes in San Francisco and Los Angeles saw the biggest price reductions in the fourth quarter, at 8.5 percent. However, these markets are also two of the most expensive for new construction homes. The typical new home with a price cut in Los Angeles cost $2 million even after its price dropped.

“More newly built homes are seeing their list prices drop, but the size of those price cuts has been remarkably steady which suggests that the trend we are seeing is being driven more by price discovery than by desperate sellers,” said Zillow Senior Economist Aaron Terrazas. “The housing market cooled in late 2018, particularly at higher price points and in pricier communities where new construction has clustered in recent years. Facing high and rising construction costs, builders have few options but to target upmarket while homebuyers are increasingly squeezed by tight affordability and rising interest rates. But the trend could be short-lived. New home building inched upward for most of the past few years, but about a year ago permitting activity began to pull back. With fewer new homes in the pipeline, these price cuts may prove to be a fleeting phenomenon.”

New construction homes are often more expensive than existing homes, and the upper price range of homes has seen more of a slowdown than the more affordable sector of the market, as demand for affordable housing keeps pressure on prices. Home value appreciation for homes in the most expensive third of the market is growing at about half the pace of the most affordable third of the market. Higher-valued homes were also more likely to have a price cut than the most affordable homes, according to previous Zillow research.

Zillow

Zillow is the leading real estate and rental marketplace dedicated to empowering consumers with data, inspiration and knowledge around the place they call home, and connecting them with great real estate professionals. In addition, Zillow operates an industry-leading economics and analytics bureau led by Zillow Group’s Chief Economist Dr. Svenja Gudell. Dr. Gudell and her team of economists and data analysts produce extensive housing data and research covering more than 450 markets at Zillow Real Estate Research. Zillow also sponsors the quarterly Zillow Home Price Expectations Survey, which asks more than 100 leading economists, real estate experts and investment and market strategists to predict the path of the Zillow Home Value Index over the next five years. Launched in 2006, Zillow is owned and operated by Zillow Group, Inc. (NASDAQ: Z and ZG), and headquartered in Seattle.

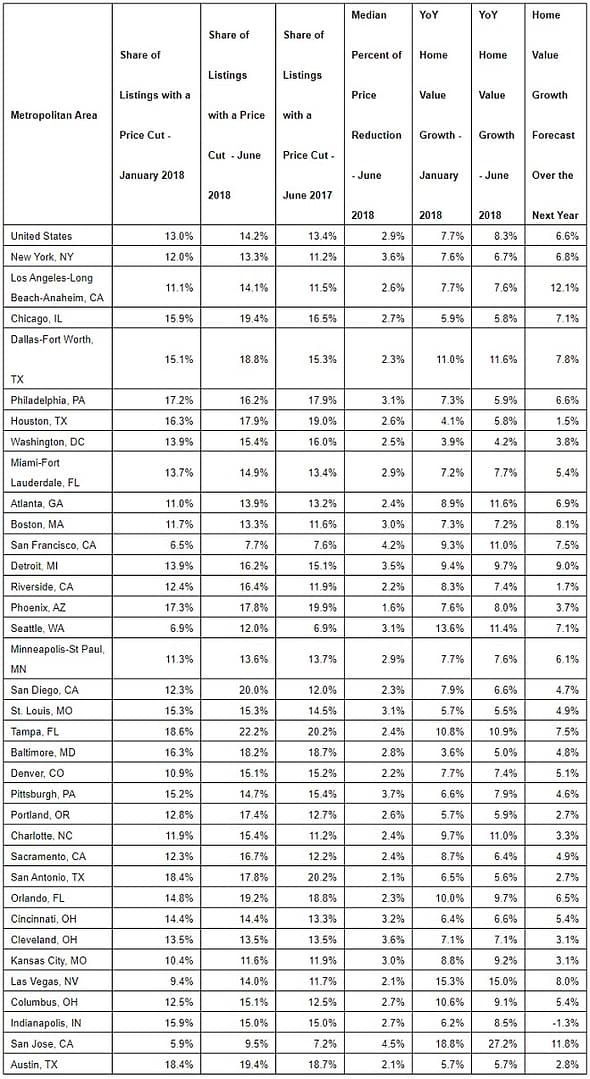

– There are more price cuts now than a year ago in over two-thirds of the nation’s largest metros, with West Coast markets reporting the greatest increase

– About 14 percent of all listings across the U.S. had a price cut in June 2018, up from a recent low of 11.7 percent near the end of 2016.

– In San Diego, 20 percent of listings had a price cut in June, up from 12 percent a year ago.

– Home value growth is slowing in almost half of the 35 largest U.S. metros, with Sacramento and Seattle reporting the greatest slowdown since the beginning of the year.

– U.S. home values rose 8.3 percent over the past year, and Zillow expects home value growth to slow to a 6.6 percent appreciation rate by this time next year.

Seattle, WA – Aug. 16, 2018 (PRNewswire) The share of home listings with a price cut is greater now than a year ago in two-thirds of the nation’s largest housing markets, according to a new Zillow® analysis. The share of listings with a price cut increased the most in markets along with West Coast, with the median amount of the price cut remaining steady across the U.S. for the past several years, at about 3 percent.

![]()

In San Diego, 20 percent of all listings had a price cut in June 2018, up from 12 percent a year ago. In Seattle, still one of the nation’s fastest appreciating housing markets despite a recent slowdown, 12 percent of all listings had a price cut in June, the greatest share since October 2014. Portland, Sacramento, Calif. and Riverside, Calif. also experienced an increase in the share of listings with a price cut compared to a year ago.

The share of listings with a price cut is on the rise across the U.S., as well. About 14 percent of all listings had a price cut in June, up from a recent low of 11.7 percent at the end of 2016. Since the beginning of the year, the share of listings with a price cut increased 1.2 percentage points, the greatest January-to-June increase ever reported, and more than double the January-to-June increase last year.

Nationally, price cuts are more common among higher-priced listings. The share of higher-priced listings with a price cut rose 0.9 percentage points since the beginning of the year, to 16.2 percent, while the share of lower-priced listings with a price cut fell 0.1 percentage points, to 11.2 percent. Higher-priced listings have seen a disproportionately large increase in price cuts in 23 of the 35 largest metros since the beginning of the year.

U.S. home values rose 8.3 percent over the past year to a median home value of $217,300. While home value growth isn’t slowing down nationally, it is slowing in some of the nation’s hottest housing markets. In almost half of the 35 largest markets, home value growth is appreciating more slowly now than at the beginning of the year. The median home value in Seattle rose 11.4 percent over the past year, but the annual growth rate was close to 14 percent at the beginning of the year.

“The housing market has tilted sharply in favor of sellers over the past two years, but there are very early preliminary signs that the winds may be starting to shift ever-so-slightly,” said Zillow senior economist Aaron Terrazas. “A rising share of on-market listings are seeing price cuts, though these price cuts are concentrated at the most expensive price-points and primarily in markets that have seen outsized price gains in recent years. It’s far too soon to call this a buyer’s market, home values are still expected to appreciate at double their historic rate over the next 12 months, but the frenetic pace of the housing market over the past few years is starting to return toward a more normal trend.”

There are fewer listings with a price cut in some of the nation’s more affordable housing markets. San Antonio, Phoenix, Philadelphia and Houston reported fewer listings with a price cut in June than a year ago. In San Antonio, where the median home value is $185,000, 17.8 percent of all listings had a price cut in June, down from about 20 percent of listings a year ago.

Zillow forecasts home value growth across the U.S. to slow to a 6.6 percent annual appreciation rate over the next year. Among the 35 largest metros, home value growth in San Jose, Calif., Indianapolis and Charlotte, N.C. are forecasted to slow the most.

Zillow

Zillow is the leading real estate and rental marketplace dedicated to empowering consumers with data, inspiration and knowledge around the place they call home, and connecting them with great real estate professionals. In addition, Zillow operates an industry-leading economics and analytics bureau led by Zillow Group’s Chief Economist Dr. Svenja Gudell. Dr. Gudell and her team of economists and data analysts produce extensive housing data and research covering more than 450 markets at Zillow Real Estate Research. Zillow also sponsors the quarterly Zillow Home Price Expectations Survey, which asks more than 100 leading economists, real estate experts and investment and market strategists to predict the path of the Zillow Home Value Index over the next five years. Launched in 2006, Zillow is owned and operated by Zillow Group, Inc. (NASDAQ: Z and ZG), and headquartered in Seattle.

Zillow is a registered trademark of Zillow, Inc.