Source: Statista

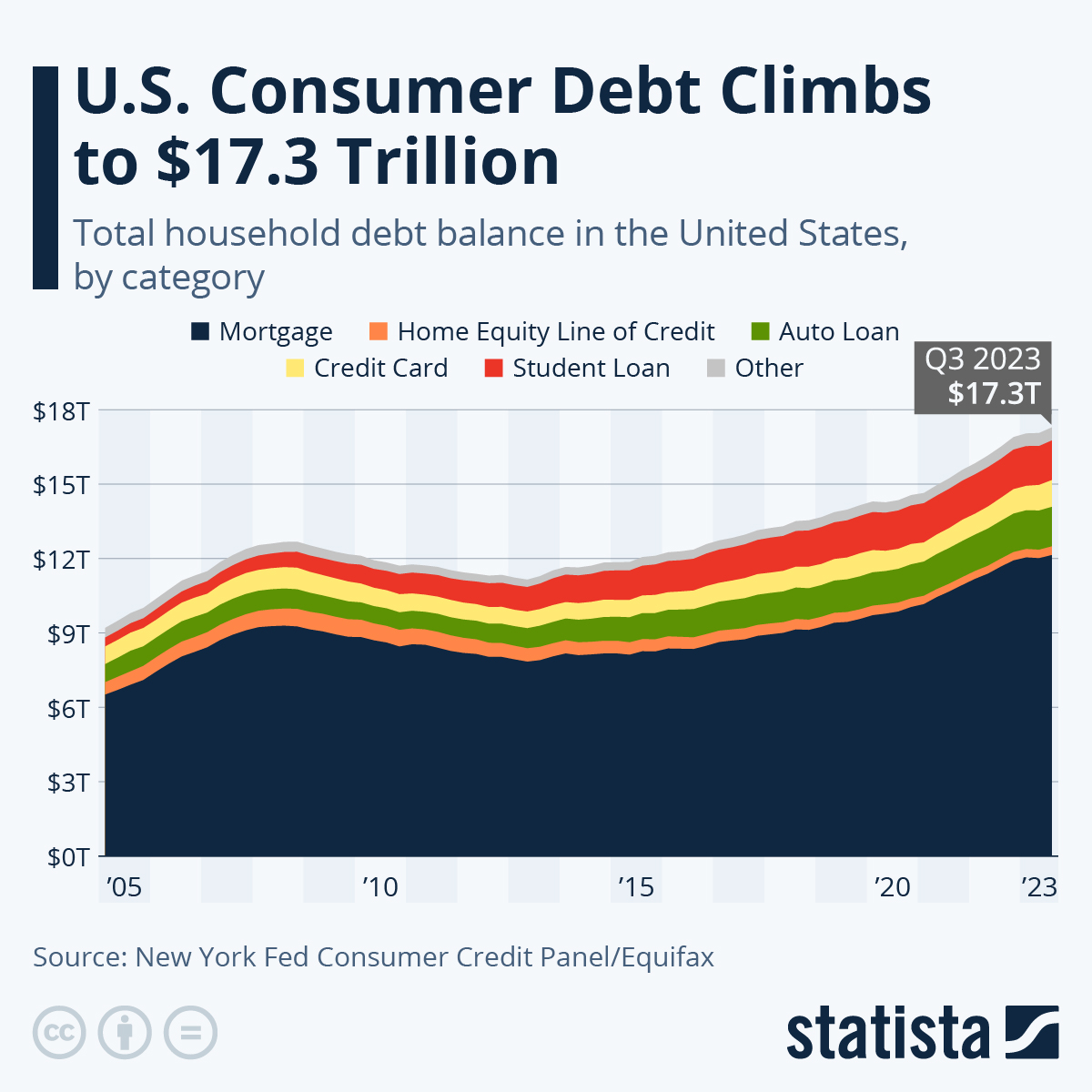

According to the New York Fed’s Quarterly Report on Household Debt and Credit, total household debt in the United States grew by $228 billion in the third quarter of 2023, to reach an all-time high of $17.3 trillion, at least in nominal terms. The increase was mainly driven by mortgage, credit card and student loan balances, which increased $126, $48 and $30 billion, respectively, with credit card debt growing the fastest in relative terms at nearly 5 percent compared to the previous quarter and 16.6 percent year-over-year.

Despite the high level of debt, overall delinquency rates remain remarkably low, despite a steady upward trend from the historic lows seen during the pandemic, when consumers were flush with cash. Looking at total consumer debt, 97 percent of the total balance was current or non-delinquent (i.e. all payments made on time or less than 30 days late) at the end of Q3 2023, up from 95.3 in Q4 2019 and from less than 90 percent in the midst of the financial crisis.

The faster-than-usual increase in consumer debt over the past three years was mainly driven by a record volume of mortgage originations, as many households took advantage of historically low rates to refinance their mortgage and even take out some cash in the process. According to the New York Fed, 14 million mortgages were refinanced during the pandemic refinancing boom, during which home owners extracted $430 billion through cash-out refinances. As a result, mortgages accounted for 82 percent of the increase in total consumer debt since Q4 2019, followed by auto loans and credit card debt, which accounted for 8 and 5 percent of the $3.1-trillion increase, respectively.