Government-sponsored enterprises play a major role in making home loans affordable for Americans; Zillow analysis examines mortgage costs if reform reduced access to government-backed mortgages

Seattle, WA – March 9, 2018 (PRNewswire) Proposed reforms to the government-sponsored enterprises (GSEs) that guarantee the majority of U.S. home loans could drive up monthly housing costs and diminish housing affordability for many Americans, according to Zillow®.

![]()

Congress is considering changes to Fannie Mae and Freddie Mac to reduce the risk to taxpayers if the housing market crashes again. The GSEs, which guarantee a majority of all home loans against defaults, have been under government conservatorship since 2008, when they required more than $150 billion in taxpayer funds as a result of foreclosures during the housing crisis.

But a Zillow analysis shows that potential changes would cost borrowers as much as $400 a month in mortgage costs.

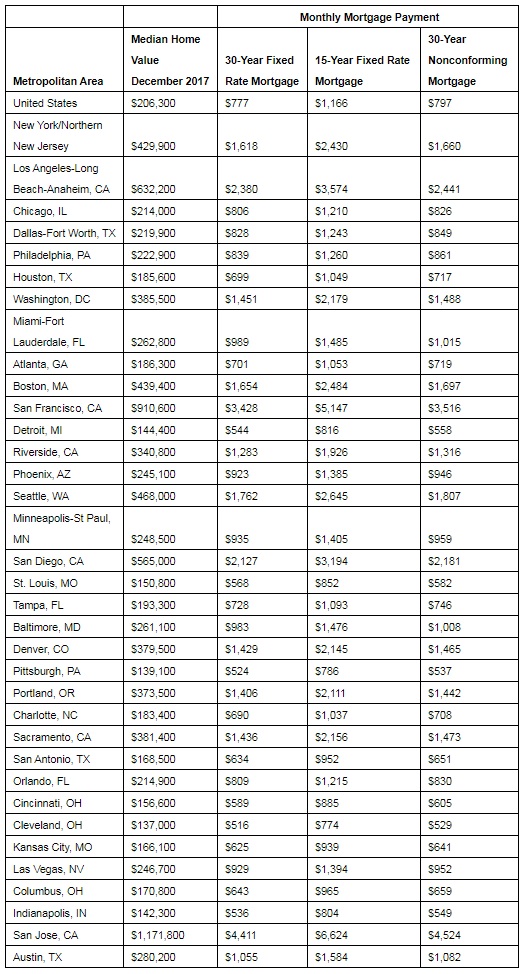

The guarantee from Fannie and Freddie is thought to keep interest rates for 30-year fixed-rate mortgages low, and housing relatively affordable. If that guarantee is changed, the typical American borrower could be facing shorter loan durations or higher rates. In this analysis, Zillow examined how alternatives to the traditional 30-year mortgage would affect borrowers’ monthly costs, using current home values and mortgage rates.

- Shorter-term loans: The typical borrower would pay an additional $390 each month on the median U.S. home for a 15-year fixed-rate mortgage instead of a 30-year loan.

- Higher rates similar to current jumbo loans(i): A 30-year non-conforming loan would cost borrowers about $20 more per month for the typical U.S. home. Jumbo, or non-conforming, loans are currently not guaranteed by GSEs.

“Some GSE reform proposals could lead to the end of the 30-year mortgage as we know it, which has long been the bedrock for financing homeownership in America,” said Zillow Senior Economist Aaron Terrazas. “If monthly payments do rise and, more importantly, stay elevated, at some point we’d expect home prices to come down a bit in response to this decreased purchasing power, and some long-time owners could opt not to sell to preserve their smaller monthly payments. A shorter loan period would mean the lifetime cost of the home is lower, and some households may be able to absorb the extra monthly cost on their mortgage. But in the nearer term, first-time homebuyers or buyers on the margin could feel a real pinch as homeownership becomes significantly less affordable.”

Until actual changes are signed into law, it is difficult to know what the typical loan will look like following GSE reform. To see the impact of other interest rates and loan durations on mortgage payments, visit Zillow Research: https://www.zillow.com/research/mortgage-payments-rates-products-18773/

Zillow

Zillow is the leading real estate and rental marketplace dedicated to empowering consumers with data, inspiration and knowledge around the place they call home, and connecting them with the best local professionals who can help. In addition, Zillow operates an industry-leading economics and analytics bureau led by Zillow’s Chief Economist Dr. Svenja Gudell. Dr. Gudell and her team of economists and data analysts produce extensive housing data and research covering more than 450 markets at Zillow Real Estate Research. Zillow also sponsors the quarterly Zillow Home Price Expectations Survey, which asks more than 100 leading economists, real estate experts and investment and market strategists to predict the path of the Zillow Home Value Index over the next five years. Launched in 2006, Zillow is owned and operated by Zillow Group, Inc. (NASDAQ: Z and ZG), and headquartered in Seattle.

(i) The current market for jumbo loans is relatively small and skewed toward the wealthy. The exact terms of today’s jumbo loans may not scale to the larger housing market.