Arch MI Spring 2018 Housing and Mortgage Market Review Finds Housing Bust Unlikely, but Mortgage Payments Expected to Be Higher

Greensboro, NC – April 12, 2018 (BUSINESS WIRE) U.S. housing became less affordable in the first quarter and the cost of carrying a mortgage could increase by the end of year – making affording a house in 2018 more difficult than it has been in decades. Specifically, U.S. housing affordability worsened by 5 percent in the first quarter of 2018 and the monthly mortgage payments needed for home purchases could go up another 10–15 percent by the end of the year, making 2018 one of the worst full-year deteriorations in affordability in the past 25 years. This assessment headlines the new Spring 2018 edition of The Housing and Mortgage Market Review (HaMMR), released today by Arch Mortgage Insurance Company (“Arch MI”).

![]()

With property location and interest rates the key factors, the cities where affordability is expected to decline the fastest include Tacoma, WA; Fresno, CA; Baltimore, MD and Boston, MA.

For homeowners, there’s good news in that home values are expected to continue to appreciate. According to the latest quarterly Arch MI Risk Index, a statistical model based on leading housing market indicators, the average probability of experiencing home price declines remains unusually low, at 5 percent. The shortage of homes for sale means that the likelihood of local housing busts, or even mild price declines, over the next two years is near historic lows. This reflects a broad array of favorable fundamentals, such as a healthy job market, relatively low interest rates and home prices in line with incomes compared to their historical norms, at least in the majority of American cities.

“If mortgage rates and home prices continue to rise as expected, affordability will get hammered by year-end as demand continues to outstrip supply,” said Dr. Ralph G. DeFranco, Global Chief Economist-Mortgage Services, Arch Capital Services Inc. “A strong U.S. economy combined with a housing shortage in many markets means that there is little hope of any price drop for buyers. Whether someone is looking to upgrade or purchase their first home, the window to buy before rates jump again is probably closing fast.”

The latest HaMMR also discusses the impact of tariffs on the housing market. While it will lead to slightly higher construction costs and a shifting of the relative economics of making steel, aluminum and final consumer goods inside and outside the U.S., it shouldn’t dent the housing market overall. Steel frames account for only a small percentage of new single-family houses, making the tariffs’ direct impact on the total cost of a new home relatively minor.

Commentary resources:

- The Housing and Mortgage Market Review (HaMMR) is posted at archmi.com/hammr. The Spring 2018 edition summarizes current U.S. housing market conditions and the effects of the latest tariffs on the housing market.

- Dr. DeFranco will host Housing Update webinars discussing market conditions and the details of HaMMR on April 19 and 20, 2018. Registration is free at archmi.com/hammr.

- Detailed and interactive regional graphs and maps showing home prices and estimates of over-/undervaluation are also available at archmi.com/hammr by clicking the HPI Charts link.

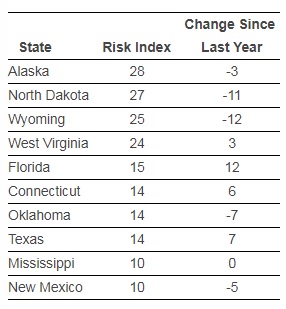

At the state level, Alaska, North Dakota, Wyoming and West Virginia have the highest probability of home price declines over the next two years. Their economies are weaker than the country overall due to the lingering effects of the unwinding of the energy-extraction boom but are expected to improve over time. According to the Arch MI Risk Index, Florida and Texas make the list of riskiest states because their home prices are higher than expected compared to the historical relationship between price and income. Given their strong housing markets, they are likely to continue moving up the list as their affordability deteriorates.

States with the Highest Risk Index Values (Probability of Price Decline Times 100)

About Arch MI’s Housing and Mortgage Market Review, Risk Index and Fundamental HVI

The Housing and Mortgage Market Review, which presents Arch MI Risk Index results, is published quarterly by Arch Mortgage Insurance Company.

The Risk Index is a proprietary statistical model that measures home price risk by estimating the probability that home prices in a state or one of the nation’s 401 largest metropolitan statistical areas (MSAs) will be lower in two years. For example, a score of 25 indicates a 25 percent chance the FHFA All-Transactions Regional Housing Price Index (HPI) will be lower in two years. The Arch MI Risk Index weights various local economic and housing market factors, such as affordability, unemployment rates, economic growth rates, net migration, housing starts, etc., based on a statistical model built on data going back to the early 1980s. It estimates the likelihood of seeing negative home prices and does not indicate the size of any declines. The latest HaMMR, Risk Index, local housing percent over-/undervaluation can be reviewed at archmi.com/hammr.

Fundamental HVI is a statistical model based on the historical relationship between incomes and home prices.

Detailed, interactive regional graphs and maps are available on Arch MI’s website, showing relative over- or undervalued home prices at archmi.com/HPI-Charts-and-Maps.

About Arch Mortgage Insurance Company

Arch Capital Group Ltd.’s U.S. mortgage insurance operation, Arch MI, is a leading provider of private insurance covering mortgage credit risk. Headquartered in Greensboro, North Carolina, with significant operations in Walnut Creek, California, Arch MI’s mission is to protect lenders against credit risk, while extending the possibility of responsible home ownership to qualified borrowers. Arch MI’s flagship mortgage insurer, Arch Mortgage Insurance Company, is licensed to write mortgage insurance in all 50 states, the District of Columbia and Puerto Rico. For more information, please visit archmi.com.

Cautionary Note Regarding Forward-Looking Statements

The Private Securities Litigation Reform Act of 1995 provides a “safe harbor” for forward-looking statements. This release or any other written or oral statements made by or on behalf of Arch Capital Group Ltd. and its subsidiaries may include forward-looking statements, which reflect our current views with respect to future events and financial performance. All statements, other than statements of historical fact included in or incorporated by reference in this release, are forward-looking statements.

Forward-looking statements can generally be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe” or “continue” or their negative or variations or similar terminology. Forward-looking statements involve our current assessment of risks and uncertainties. Actual events and results may differ materially from those expressed or implied in these statements. A non-exclusive list of the important factors that could cause actual results to differ materially from those in such forward-looking statements includes the following: adverse general economic and market conditions; increased competition; pricing and policy term trends; fluctuations in the actions of rating agencies and our ability to maintain and improve our ratings; investment performance; the loss of key personnel; the adequacy of our loss reserves, severity and/or frequency of losses, greater than expected loss ratios and adverse development on claim and/or claim expense liabilities; greater frequency or severity of unpredictable natural and man-made catastrophic events; the impact of acts of terrorism and acts of war; changes in regulations and/or tax laws in the United States or elsewhere; our ability to successfully integrate, establish and maintain operating procedures and integrate the businesses we have acquired or may acquire into the existing operations; changes in accounting principles or policies; material differences between actual and expected assessments for guaranty funds and mandatory pooling arrangements; availability and cost to us of reinsurance to manage our gross and net exposures; the failure of others to meet their obligations to us, and other factors identified in our filings with the U.S. Securities and Exchange Commission.

The foregoing review of important factors should not be construed as exhaustive and should be read in conjunction with other cautionary statements that are included herein or elsewhere. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

© 2018 Arch Mortgage Insurance Company. All Rights Reserved. Arch MI is a marketing term for Arch Mortgage Insurance Company and United Guaranty Residential Insurance Company. The Housing and Mortgage Market Review and Arch MI Risk Index are registered marks of Arch Capital Group (U.S.) or its affiliates. HaMMR is a service mark of Arch Capital Group (U.S.) or its affiliates.

Contacts

Arch Capital Services Inc.

Greg Hare

(336) 333-0416

or

Method Communications

Ramona Redlingshafer

(415) 849-1322