Suburban applicants are more likely to be approved for a conventional loan than borrowers in urban or rural areas

Seattle, WA – April 19, 2018 (PRNewswire) Mortgage applications are denied at the lowest rate in the past 20 years, yet a stark divide remains between potential homebuyers of different racial groups.

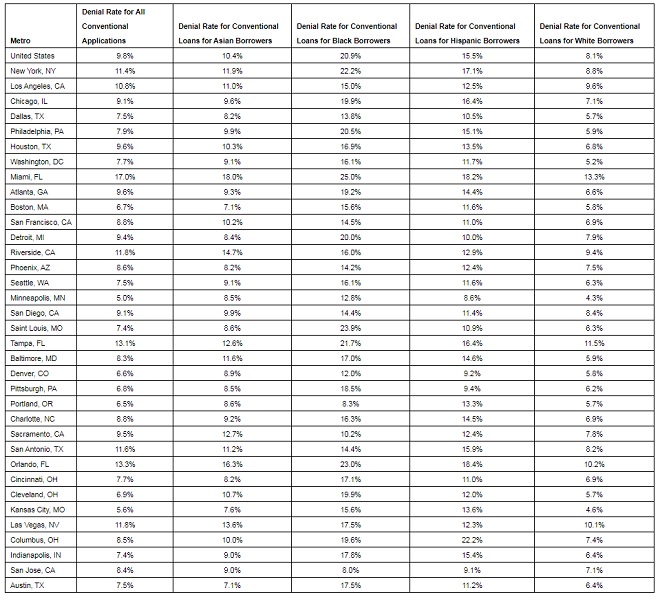

![]()

Nationally, the share of applicants who are denied for conventional mortgages has fallen to 9.8 percent, according to data from the Home Mortgage Disclosure Act (HMDA), down from 18.1 percent in 2007.

Even though a smaller share of loan applicants overall are denied, white or Asian borrowers are more likely to be approved for a mortgage than black or Hispanic borrowers. In 2016, 8.1 percent of white applicants were denied for a conventional loan, as were 10.4 percent of Asian applicants. By comparison, 20.9 percent of black borrowers and 15.5 percent of Hispanic borrowers were turned down for a loan.

For all groups, denial rates are down sharply from 2007. In 2007, 34.3 percent of black applicants and 30 percent of Hispanic applicants were denied for mortgages. White and Asian borrowers were denied 12.7 percent and 16.2 percent of the time, respectively.

The persistent disparity among races also is evident in homeownership. The gap between black and white homeownership rates was slightly wider in 2016 than it was in 1900i. Black homebuyers had the least purchasing power last year – they could afford 55 percent of homes for sale, while white homebuyers could buy about 78 percent of listed homesii. And while coming up with a down payment is the biggest hurdle to homeownership for all potential buyers, black Americans were more likely than those of other races to say qualifying for a mortgage was a barrieriii.

“Mortgage approval data point to both progress and stubborn inequities in the American housing market,” said Zillow® Senior Economist Aaron Terrazas. “By some measures, the gap in mortgage approval rates between whites and blacks is as narrow as it has ever been. However, black mortgage applicants are still more than twice as likely as whites to be denied, a visible legacy of historical discriminatory policies. For the large majority of home buyers, getting approved for a loan is the first step on the road to homeownership, and these continued disparities represent an ongoing barrier to housing and social equity in America.”

For all racial and ethnic groups, borrowers in suburban areas had the best chances of being approved for a mortgage – 8.4 percent of suburban homebuyers were denied for a loan, while 10 percent of urban borrowers and 11.5 percent of rural borrowers were turned down.

Zillow

Zillow is the leading real estate and rental marketplace dedicated to empowering consumers with data, inspiration and knowledge around the place they call home, and connecting them with the best local professionals who can help. In addition, Zillow operates an industry-leading economics and analytics bureau led by Zillow’s Chief Economist Dr. Svenja Gudell. Dr. Gudell and her team of economists and data analysts produce extensive housing data and research covering more than 450 markets at Zillow Real Estate Research. Zillow also sponsors the quarterly Zillow Home Price Expectations Survey, which asks more than 100 leading economists, real estate experts and investment and market strategists to predict the path of the Zillow Home Value Index over the next five years. Launched in 2006, Zillow is owned and operated by Zillow Group, Inc. (NASDAQ: Z and ZG), and headquartered in Seattle.

Zillow is a registered trademark of Zillow, Inc.

(i) https://www.zillow.com/research/homeownership-gap-widens-19384/

(ii) https://www.zillow.com/research/affordable-home-listings-by-race-19419/

(iii) Zillow Housing Aspirations Report, September 2017