In the following video, from the Inman News YouTube channel, Sherry Chris, CEO of Better Homes and Gardens, talks with Google’s Matt Lawson about the importance of the little things that often slip between the cracks.

In the following video, from the Inman News YouTube channel, Sherry Chris, CEO of Better Homes and Gardens, talks with Google’s Matt Lawson about the importance of the little things that often slip between the cracks.

LendingTree’s Consumer Debt Outlook finds credit card balances still below 2008 levels; student loan debt levels continue to balloon

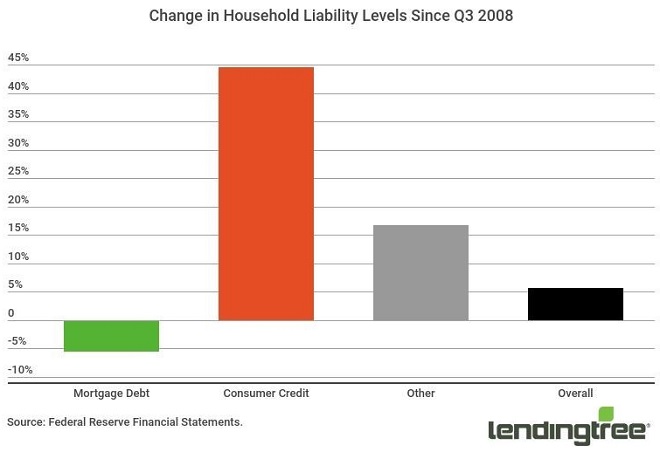

Charlotte, NC – June 21, 2018 (PRNewswire) LendingTree®, the nation’s leading online loan marketplace, today released its Consumer Debt Outlook for June 2018, finding that American household debt is currently on pace to exceed the prior peak debt level from 2008 by the end of June, primarily due to non-mortgage consumer debt. LendingTree’s analysis of the latest Federal Reserve data found that mortgage-related household debt has actually fallen by 5.5 percent while total consumer credit – a collection of revolving credit and installment loans – has increased by 45 percent, of which 42 percent is comprised of student debt alone.

Analysis Highlights

Household debt to surpass 2008 peak by $1 trillion

In the first quarter of this year, household net worth, as measured by the Federal Reserve Financial Accounts, reached $100 trillion for the first time. Assets — primarily financial instruments and real estate — gained more than $1.07 trillion in the first quarter, handily outpacing the additional debt Americans accumulated.

Nonetheless, liabilities have been steadily increasing in recent years. But unlike a decade ago, mortgages aren’t the culprit. It is non-mortgage-related debt, such as student loans, credit card debt and auto loans, that have been growing. By the end of the second quarter 2018, we’ll have $1 trillion more in household debt than we did in 2008 — and none of it is attributable to housing.

Since the third quarter of 2008, the peak of last decade’s housing bubble, mortgage-related household debt has actually fallen by 5.5 percent. Meanwhile, consumer credit — a collection of revolving credit and installment loans, has increased by 45 percent.

Credit card balances still below 2008 levels; student loan debt levels continue to balloon

Consumer credit is a collection of a number of household liabilities — auto loans, credit cards and student loans are the three largest types. Of the three, student loan balances are growing the fastest — they’ve risen 130 percent since the housing crisis began. Compare that with auto loans, which have risen a much more modest 39 percent in the past decade. Credit card balances are actually slightly lower than they were in 2008, and that’s before factoring in 10 years of inflation.

In other words, over the past decade, the burden of non-mortgage debt has shifted from credit card borrowers to student loan borrowers. Credit cards and student loans have switched places. In 2008, credit card debt comprised 40 percent of household liabilities, and student loan debt made up 27 percent. Today, those shares are swapped — student loans make up 42 percent of the nation’s household debt, and credit cards are now only 28 percent of the share.

But no matter the mix, the trend is definitely more debt. LendingTree analysts project that total consumer debt (excluding mortgage debt) will exceed $4 trillion by the end of 2018.

Income gains are mitigating the increase for most; millennials are an exception

Although total household debt has returned to 2008 levels, the difference in 2008 and today’s income and types of debt are significant.

Most important, mortgage balances as a percentage of disposable personal income has fallen from a high of 98 percent in 2008 to 68 percent as of the latest quarter. In other words, homeowners today, on average, have significant equity in their homes. Ten years ago, equity was virtually nonexistent.

Similarly, credit card debt, as measured as a percentage of income, has fallen by about 30 percent versus the levels they were at a decade earlier. Credit card balances represent about 6.6 percent of income as of the first quarter of 2018; a decade ago, it was nearly 9 percent.

At the other end of the spectrum, student loan borrowers are shouldering nearly 70 percent more than they were a decade ago, as student loans now represent 10.3 percent of disposable income, versus 6 percent a decade ago.

As millennials bear most of this student loan debt while remaining underrepresented in homeownership versus other age cohorts, the economic distress of millennials becomes much more understandable, at least on a relative basis, and relating specifically to debt burdens.

To view the full report, visit: www.lendingtree.com.

About LendingTree

LendingTree (NASDAQ: TREE) is the nation’s leading online loan marketplace, empowering consumers as they comparison-shop across a full suite of loan and credit-based offerings. LendingTree provides an online marketplace which connects consumers with multiple lenders that compete for their business, as well as an array of online tools and information to help consumers find the best loan. Since inception, LendingTree has facilitated more than 65 million loan requests. LendingTree provides free monthly credit scores through My LendingTree and access to its network of over 500 lenders offering home loans, personal loans, credit cards, student loans, business loans, home equity loans/lines of credit, auto loans and more. LendingTree, LLC is a subsidiary of LendingTree, Inc. For more information go to www.lendingtree.com, dial 800-555-TREE, like our Facebook page and/or follow us on Twitter @LendingTree.

MEDIA CONTACT:

Megan Greuling

(704) 943-8208

megan.greuling@lendingtree.com

Washington, D.C. – April 24, 2018 (nar.realtor) As consumer demand trends toward green and sustainable home features, Realtors® continue to work to promote environmentally responsible features and business practices. Sixty-one percent of Realtors® reported that consumers are interested in sustainability according to the National Association of Realtors®’ REALTORS® and Sustainability 2018 report.

![]()

The report, www.nar.realtor/research-and-statistics/research-reports/realtors-and-sustainability, which stems from NAR’s Sustainability Program, surveyed Realtors® about sustainability issues in the residential and commercial real estate markets and the preferences they are seeing in consumers in their communities.

“Consumers continue to make it clear that environmentally friendly features and neighborhoods are an important factor in deciding where and what home to buy,” said NAR President Elizabeth Mendenhall, a sixth-generation Realtor® from Columbia, Missouri and CEO of RE/MAX Boone Realty. “Realtors® are leaders in the conversation about real estate sustainability, energy conservation and resource efficiency, and will continue to promote environmentally conscious strategies and best practices that benefit not just our clients, but also our communities.”

Seventy-one percent of agents and brokers reported that promoting energy efficiency in listings is either somewhat or very valuable. When asked what they consider to be the top market issues and considerations regarding sustainability, agents and brokers listed understanding lending options for energy upgrades or solar panels (36 percent), improving the energy efficiency of existing housing stock (34 percent) and the lack of information and materials provided to real estate professionals (30 percent).

The survey asked Realtors® how comfortable they are answering questions about home performance and efficiency; 39 percent said they are comfortable or extremely comfortable. Forty percent of respondents say they are confident or extremely confident in their ability to connect clients with green lenders.

To account for growing consumer interest, 40 percent of respondents reported that their Multiple Listing Service, or MLS, have green data fields, compared to only 15 percent that do not. Among those that do have green data fields, 37 percent of respondents use them to promote green features, 27 percent to promote energy information and 16 percent to promote green certifications.

A majority of respondents (80 percent) said that solar panels are available in their market, and 39 percent said that solar panels increased the perceived property value. Twenty-three percent of brokers indicated that tiny homes – homes that are 600 square feet or less – are available in their market.

The transportation and commuting features that Realtors® stated are very or somewhat important to their clients include easy access to highways (82 percent), short commute times and distance to work (81 percent) and walkability (51 percent).

For the first time questions about commercial real estate were included in the survey. Seventy percent of agents and brokers indicated that promoting energy efficiency in their commercial listings was very or somewhat valuable. The top building features that clients specified as very or somewhat important to their agents or brokers are utility/operation costs (80 percent), efficient use of lighting (64 percent) and indoor air quality (62 percent).

NAR initiated the Sustainability Program as a platform for dialogue on sustainability for Realtors®, brokers, allied trade associations, and consumers. The program’s efforts focus on coordination and articulation of NAR’s existing sustainability resources, while also supporting a growing area of interest for consumers, helping members to assist home buyers and sellers.

The REALTOR® Sustainability Program invited a sample of 112,220 active Realtors® to participate in an online survey pertaining to sustainability issues facing consumers and the industry, resulting in 6,834 usable responses. NAR plans to use this report to better benchmark Realtor® understanding of sustainability and create resources to help Realtors® better serve clients surrounding sustainability topics.

The National Association of Realtors®, “The Voice for Real Estate,” is America’s largest trade association, representing 1.3 million members involved in all aspects of the residential and commercial real estate industries.