Despite rising mortgage rates and slower sales, home prices to rise at a healthier pace in 2018 and beyond

Washington, D.C. – Aug. 27, 2018 (PRNewswire) American financial and lending systems look vastly different nearly a decade after the defining moments of the Great Recession, thanks in part to safe and sound lending and regulatory policy reforms, strongly supported by the National Association of Realtors®. Today, home prices are at or approaching record highs in many markets, and mortgage default and foreclosure rates sit near historic lows.

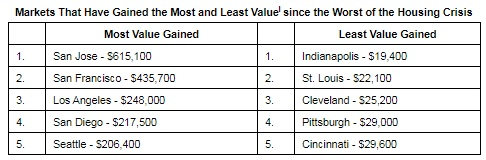

![]()

Overall, the housing market has recovered from the financial crisis that began ten years ago, as the nation’s homeownership rate continues to inch higher. And although some regions have experienced sales declines in recent months, NAR Chief Economist Lawrence Yun says concerns about whether the housing market has peaked and is headed for another significant slowdown are unfounded.

He believes some of the nation’s most overheated real estate markets will see sales slowdown in 2018, but notes those are occurring because of insufficient supply and rapidly rising home prices rather than weak buyer demand, a more reliable indicator of a true slowdown. This is a much better problem to have than a shortage of demand, which remains high across much of the country, says Yun.

Lawrence Yun

Realtors® across the country have stated that limited housing inventory is hindering local market home sales. Inventory levels have fallen for three straight years, and multiple bidding is still prevalent on starter homes in many markets across the country. Some of the nation’s hottest housing markets – which include cities like Seattle and Denver – are said to be slowing, but drops in homes sales can be connected directly to supply shortages and corresponding price increases.

“The answer is to encourage builders to increase supply, and there is a good probability for solid home sales growth once the supply issue is addressed,” Yun said. “Additional inventory will also help contain rapid home price growth and open up the market to perspective homebuyers who are consequently – and increasingly – being priced out. In the end, slower price growth is healthier price growth.”

While homebuilding increased 7.2 percent year-to-date to July, Yun contends that even more construction is needed to fill national shortages. Some unavoidable barriers stand in the way, but more deliberate and well intentioned policy decisions can help alleviate the housing shortages facing markets across the country.

“Rising material costs and labor shortages do not help builders to be excited about business,” Yun said. “But the lumber tariff is a pure, unforced policy error that raises costs and limits job creations and more home building.”

As a result of those headwinds, Yun forecasts existing-home sales in 2018 to decrease 1.0 percent to 5.46 million – down from 5.51 million in 2017. Despite the expected drop in sales in some markets, home price growth should remain strong in markets across the country and increase about 5 percent on a nationwide basis.

In 2019, with anticipated rise in inventory and moderate price growth, home sales should remain higher. Existing home sales are forecast to rise 2 percent in 2019, while home prices are expected to rise by 3.5%, Yun said.

The National Association of Realtors®, “The Voice for Real Estate,” is America’s largest trade association, representing 1.3 million members involved in all aspects of the residential and commercial real estate industries.

Information about NAR is available at www.nar.realtor. This and other news releases are posted in the “News, Blogs and Videos” tab on the website.