Real Estate Sales – Is It All in the Agents Name? Posted on May 10, 2017 by Admin Reply If you enjoyed this post you’ll certainly enjoy these other ‘Just For Fun’ posts! Share this:FacebookTwitterPinterestEmailLinkedInRedditLike this:Like Loading...

The Perfect Product for Real Estate Inspections – Introducing Presto Inspecto! Posted on May 10, 2017 by Admin Reply If you enjoyed this post you’ll certainly enjoy these other ‘Just For Fun’ posts! Share this:FacebookTwitterPinterestEmailLinkedInRedditLike this:Like Loading...

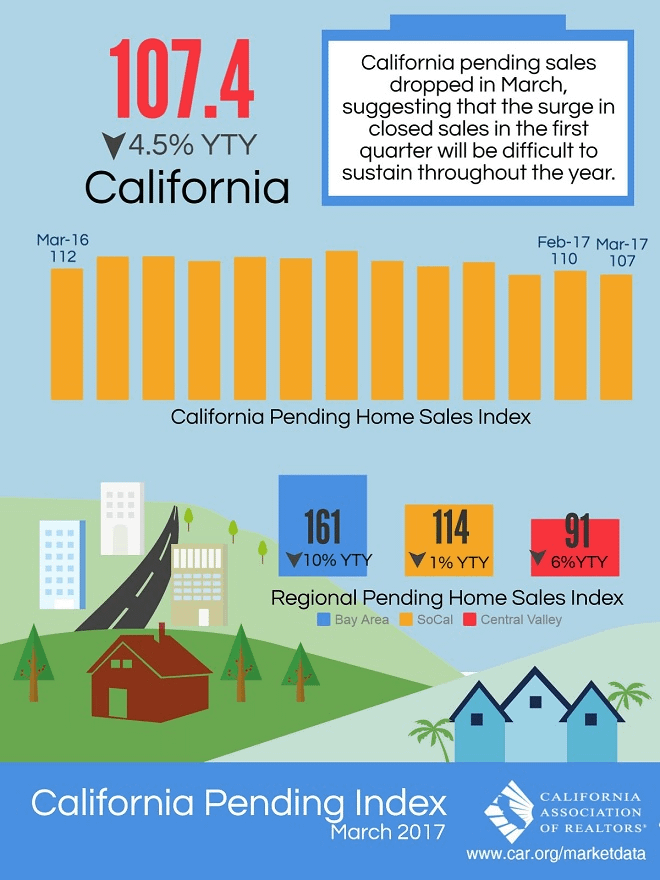

California Pending Home Sales Index – March 2017 (Infographic) Posted on May 10, 2017 by Admin Reply Share this:FacebookTwitterPinterestEmailLinkedInRedditLike this:Like Loading...