LendingTree’s Chief Economist analyzes December’s mortgage offers

Charlotte, NC – Jan. 9, 2019 (PRNewswire) LendingTree®, the nation’s leading online loan marketplace, today released its monthly Mortgage Offers Report, which analyzes data from actual loan terms offered to borrowers on LendingTree.com by lenders on LendingTree’s network. The purpose of the report is to empower consumers by providing additional information on how their credit profile affects their loan prospects.

![]()

- December’s best mortgage offers for borrowers with the best profiles had an average APR of 4.35% for conforming 30-year, fixed-rate purchase loans, down from 4.66% in November. The APR on refinance loan offers also decreased from 4.63% in November to 4.34%. We consider people with the best credit profiles to be those in the 95th percentile of borrowers who received the best mortgage offers through the LendingTree marketplace, which allows users to compare offers from multiple mortgage lenders.

- Mortgage rates vary depending upon parameters including credit score, loan-to-value ratio, income and property type.

For the average borrower, the purchase APR for conforming 30-year, fixed-rate purchase loans offered on LendingTree’s platform was 5.17%, down 18 basis points from November. The loan note rate of 5.05% was down 19 basis points from November. We prefer to emphasize the APR as lenders often make changes to other fees in response to changing interest rates. - Consumers with the highest credit scores (760+, representing the 65th percentile of borrowers) received an average APR of 4.98%, versus 5.33% for consumers with scores of 680 to 719. The APR spread of 65 basis points between these score ranges is higher than it was in November. For the average purchase loan amount of $224,609, the spread represents over $17,000 in additional costs for borrowers with lower credit scores over 30 years. The additional costs result from higher interest rates, larger fees or a combination of the two.

- For the average borrower, the APR for conforming 30-year, fixed-rate refinance loans decreased 24 basis points from November to 5.09%. At 4.93% and 5.21%, respectively, the spread between credit score brackets (760+ and 680-719) was 28 basis points. That amounts to nearly $13,000 in extra costs over the life of the loan for borrowers with lower credit scores, given an average refinance loan of $239,329.

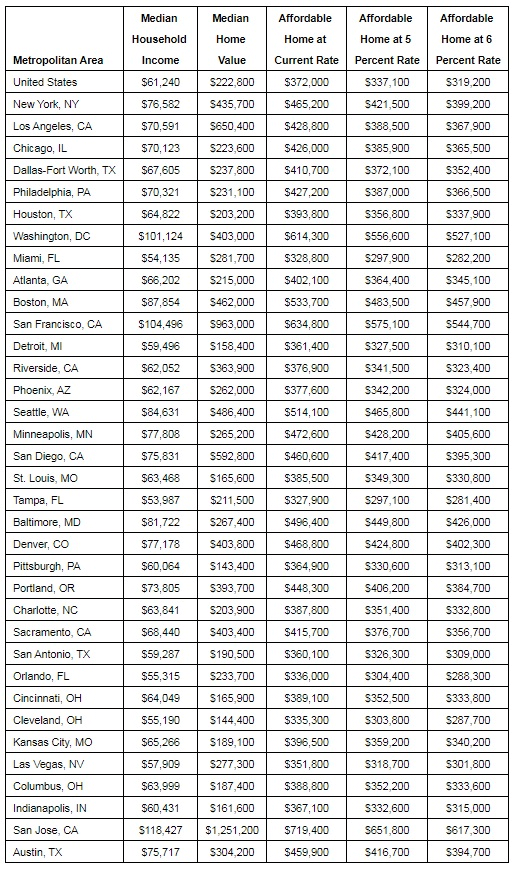

- Average proposed purchase down payments fell to $54,217, a decline of nearly $6,000.

Purchase APR by Credit Score Range

* Lifetime interest paid is calculated based on the overall average loan amount to enable comparison.

*Lifetime interest paid is calculated based on the overall average loan amount to enable comparison.

To view the Mortgage Offers Report, visit: www.lendingtree.com.

LendingTree also released its weekly Mortgage Comparison Shopping Report, containing the Mortgage Rate Distribution and Mortgage Rate Competition Index. This week’s report found that 80.9 percent of purchase borrowers received mortgage rates under 5 percent last week. Homebuyers could have seen median lifetime savings of $30,377 in interest on a $300,000 loan by comparison shopping for the best mortgage rates.

About the Report

The LendingTree Mortgage Offers Report contains data from actual loan terms offered to borrowers on LendingTree.com by lenders. We believe it is an important addition to standard industry surveys and reports on mortgage rates. Most quoted industry rates are for a hypothetical borrower with prime credit who makes a 20% down payment. Most borrowers do not fit this profile. Our report includes the average quoted APR by credit score, together with the average down payment and other metrics described below. We stratify by credit score, so borrowers have added information on how their credit profile affects their loan prospects. The report covers conforming 30-yr fixed loans for both purchase and refinance.

- APR: Actual APR offers to borrowers on our platform

- Down Payment: Though analogous to the LTV, we find that borrowers identify more closely with the down payment. Academic studies have also found that the down payment is the primary concern for homebuyers and one of the main impediments to entering the homebuying market.

- Loan Amount: The average loan amount borrowers are offered

- LTV: Actual LTV offered to borrowers on our platform

- Lifetime Interest Paid: This is the total cost a borrower incurs for the loan, inclusive of fees.

About LendingTree

LendingTree (NASDAQ: TREE) is the nation’s leading online marketplace that connects consumers with the choices they need to be confident in their financial decisions. LendingTree empowers consumers to shop for financial services the same way they would shop for airline tickets or hotel stays, comparing multiple offers from a nationwide network of over 500 partners in one simple search, and can choose the option that best fits their financial needs. Services include mortgage loans, mortgage refinances, auto loans, personal loans, business loans, student refinances, credit cards and more. Through the My LendingTree platform, consumers receive free credit scores, credit monitoring and recommendations to improve credit health. My LendingTree proactively compares consumers’ credit accounts against offers on our network, and notifies consumers when there is an opportunity to save money. In short, LendingTree’s purpose is to help simplify financial decisions for life’s meaningful moments through choice, education and support. LendingTree, LLC is a subsidiary of LendingTree, Inc. For more information, go to www.lendingtree.com, dial 800-555-TREE, like our Facebook page and/or follow us on Twitter @LendingTree.

Media Contact:

Megan Greuling

(704) 943-8208

Megan.greuling@lendingtree.com