NRMLA/RiskSpan Reverse Mortgage Market Index Hits All-Time High of 271.58

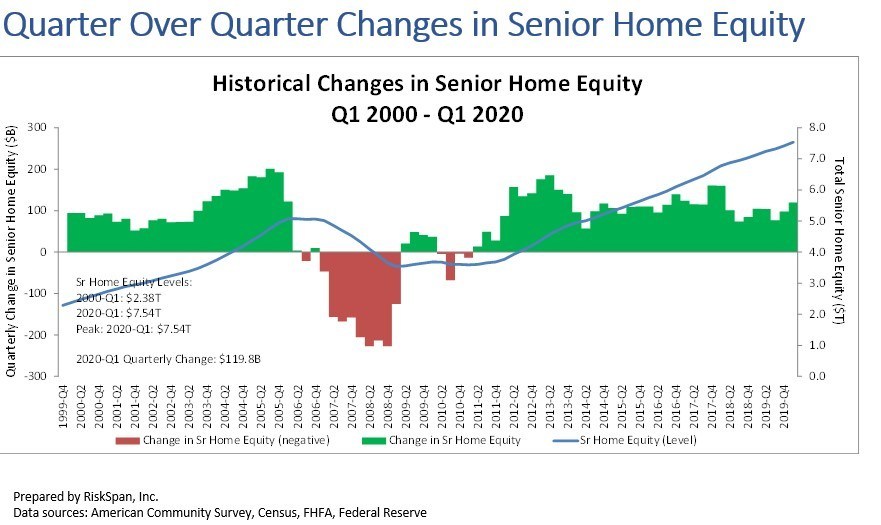

Washington, D.C. – June 26, 2020 (PRNewswire) Homeowners 62 and older saw their housing wealth grow by 1.6 percent or $120 billion in the first quarter to a record $7.54 trillion from Q4 2019, the National Reverse Mortgage Lenders Association reported today in its quarterly release of the NRMLA/RiskSpan Reverse Mortgage Market Index.

(PRNewsfoto/National Reverse Mortgage Lende)

The RMMI rose in Q1 2020 to 271.58, another all-time high since the index was first published in 2000. The increase in senior homeowner’s wealth was mainly driven by an estimated 1.4 percent or $132 billion increase in senior home values, offset by a 0.7 percent or $12.3 billion increase in senior-held mortgage debt.

“COVID-19 has impacted millions of families and their retirement portfolios, and a new study from the Center for Retirement Research at Boston College indicates that market shocks are a growing concern for many families whose retirement assets are in 401(k)s,” says NRMLA President Steve Irwin. “The responsible use of home equity may be an option to help mitigate certain market risks and help seniors stay financially secure during future market disruptions.”

About Reverse Mortgages Reverse mortgages are available to homeowners age 62 and older with significant home equity. They are a versatile financial tool that seniors can use to borrow against the equity in their home without having to make monthly principal or interest payments as with a traditional “forward” mortgage or a home equity loan. Under a reverse mortgage, funds are advanced to the borrower and interest accrues, but the outstanding balance is not due until the last borrower leaves the home, sells or passes away.

To date, more than 1.17 million households have utilized an FHA-insured reverse mortgage to help meet their financial needs. For more information, please visit www.ReverseMortgage.org

About the National Reverse Mortgage Lenders Association The National Reverse Mortgage Lenders Association (NRMLA) is the national voice for the industry and represents the lenders, loan servicers, and housing counseling agencies responsible for more than 90 percent of reverse mortgage transactions in the United States. All NRMLA member companies commit themselves to a Code of Ethics & Professional Responsibility. Learn more at www.nrmlaonline.org.

About RiskSpan, Inc. RiskSpan offers end-to-end solutions for data management, risk management analytics, and visualization on a highly secure, fast, and fully scalable platform that has earned the trust of the industry’s largest firms. Combining the strength of subject matter experts, quantitative analysts, and technologists, the RiskSpan platform integrates a range of data-sets–including both structured and unstructured–and off-the-shelf analytical tools to provide you with powerful insights and a competitive advantage. Learn more at www.riskspan.com.

Contact: Darryl Hicks, 202-939-1784, dhicks@dworbell.com National Reverse Mortgage Lenders Association

SOURCE National Reverse Mortgage Lenders Association

1 in 6 Black mortgage applicants is denied nationwide, compared to 1 in 14 white applicants – and the gap is even wider in the most segregated parts of the country

Banks most frequently cite debt and credit history when denying Black applicants, but bias in lending also plays a role

Seattle, WA – July 6, 2020 (PRNewswire) (NASDAQ: RDFN) — 15.9% of Black Americans who apply for mortgages are rejected nationwide, compared with just 7% of white Americans, according to a Redfin (www.redfin.com) analysisof Home Mortgage Disclosure Act data from the Consumer Financial Protection Bureau (CFPB). The gap is widest in Milwaukee, San Francisco, Detroit, Chicago and St. Louis, where denial rates for Black homebuyers are more than 10 percentage points higher than they are for white homebuyers. In Milwaukee and San Francisco, specifically, Black loan seekers are more than three times as likely to be denied a mortgage.

“Getting denied a loan serves a huge blow to a person’s self esteem—especially for people of color, who often feel like the world is already falling on them,” said Brittani Walker, a Redfin agent in Chicago. “My mother has been a renter since she moved out of her parents’ house. I tried to get her pre-approved for a mortgage a couple of years ago, but she was rejected because she had some blemishes on her credit. She broke down in tears and hasn’t tried again since. When people of color are stuck in this cycle of renting, their children often meet the same fate, missing out on thousands of dollars worth of home equity. If your parents never owned a home, where do you learn the value of homeownership?”

Overall, Americans today are half as likely to be denied a mortgage loan as they were in the wake of the 2008 financial crisis. The share of total applicants who faced rejection dropped to 8.9% in 2019 from 18% in 2008, according to the latest annual figures just released by the CFPB. Still, Black loan seekers are more frequently denied due to debt and low credit scores. These two factors are more likely to be roadblocks for Black mortgage applicants due to decades of wealth inequality, as well as bias among lenders.

While the racial mortgage gap has been narrowing over the years, Black Americans are still denied home loans at a higher rate than white Americans in every one of the 50 most populous U.S. metros.

Metros with the Largest and Smallest Gaps Between Black and White Denial Rates In Milwaukee, 19.5% of Black mortgage applicants are rejected, compared with just 4.8% of white applicants. In other words, Black applicants are four times more likely to face rejection. Milwaukee’s 14.7-percentage-point gap represents the biggest disparity among the top 50 metros. San Francisco has the second largest gap (19.2% vs 5.9%; 13.3 percentage points), followed by Detroit (20.3% vs 7.2%; 13.1 percentage points), Chicago (18.5% vs 5.7%; 12.8 percentage points) and St. Louis (18.1% vs 5.6%; 12.5 percentage points).

Milwaukee is the most segregated metro in the nation—with almost 90% of African Americans living in the inner city—while Chicago, Detroit and St. Louis are the third, fourth and sixth most segregated. Milwaukee also has the second-lowest Black homeownership rate of any metro in the U.S. Just 27% of Black families there own their homes, compared with 70% of white families—13 percentage points wider than the national gap.

“The residue of redlining is still very tangible in Milwaukee and Chicago,” said Arnell Brady, a Redfin Mortgage adviser who represents both cities. “Segregation continues to perpetuate the uneven playing field for Black communities, which are severely underserved when it comes to financial education and access to credit. Buying a home isn’t like walking into a bank and getting a credit card. Everyone wants a piece of the American dream, but that’s hard to achieve when you don’t have access to the right tools and information.”

Meanwhile, the metro with the smallest gap is San Diego, where 10.8% of Black mortgage applicants are rejected, compared with 7.3% of white applicants, making for a difference of just 3.5 percentage points. In second place is Seattle (10% vs 5.2%; 4.8 percentage points), followed by Sacramento (11.2% vs 6.2%; 5 percentage points), Anaheim (13.2% vs 8.1%; 5.1 percentage points) and Las Vegas (13.7% vs 8.1%; 5.6 percentage points).

Reasons for Denial While debt is the number-one explanation lenders provide when denying applicants across races, Black homebuyers are more frequently turned down for this reason, according to the CFPB. Of Black mortgage applicants who are refused home loans, 32.5% are turned away because of their debt-to-income ratios versus 27.9% of white applicants.

In a Redfin survey from February 2020, 45% of the 232 Black respondents said that student debt, specifically, stopped them from trying to buy a home sooner. That compared with 31% of white respondents.

The discrepancy is even more stark when it comes to credit, with a quarter of Black applicants being shown the door due to their credit histories, versus just 18.5% of white applicants. Research has shown that the algorithms many lenders now use in credit scoring, which are meant to be unbiased, may actually systematically deny credit access to specific groups.

Lender Discretion While banks often cite debt or a low credit score as the reason for denying mortgages to Black Americans, biases held by lenders also play a part.

“Banks still have a lot of power when it comes to determining who gets a loan,” Brady said. “Black applicants are more likely to be asked to provide additional documents despite very clear guidelines from federal agencies on what’s required. I’m a mortgage adviser who knows the rules backward and forward, and I’ve encountered this as a loan-applicant myself. Why are you asking me for two years of tax returns when the requirement is one?”

One way to curtail this discrimination would be to hide applicant names and races/ethnicities from underwriters when they are determining risk, according to Elizabeth Korver-Glenn, an assistant professor at the University of New Mexico.

Another problem is the lack of incentive to help clients with low credit scores, Brady added. Loan officers in the industry are more likely to offer advice to a borrower who already has a high FICO score and just wants to secure a better interest rate than to help someone who needs to increase their score to the 620 minimum just so they qualify for a loan, he said.

Opportunities for Change Beyond providing bias training and incentivizing mortgage brokers to lend money to people of color and low-income Americans, there are countless ways to even the playing field. For example, offering more homebuyer classes and financial education in minority communities could help more people of color realize homeownership is within their means.

“Many people aren’t aware that you don’t need a 20% down payment or a 750 credit score to buy a house,” Walker said. “There are down payment assistance programs that buyers can take advantage of, but they have higher interest rates. Luckily, you can refinance out of those higher rates, but in order to do that, you need to understand refinancing.”

Diversifying hiring within the mortgage and real estate industries is another way to help ensure that underserved communities have advocates to educate and guide them through the loan application and homebuying processes. Just 26.4% of workers in the housing industry identify as a racial or ethnic minority, according to Fannie Mae.

Alternative credit-scoring models could also help combat the racial mortgage gap. For instance, credit agencies could value on-time rent payments the same way they value on-time mortgage payments, helping more renters prove their creditworthiness. They could also place more emphasis on job stability, said Jason Bateman, head of Redfin Mortgage.

“If you’ve worked for the post office for 20 years, that should be scored higher than working for a startup out of someone’s garage for two months,” he said. “The post office is going to be here 10 years from now, but the startup in the garage might not be.”

About Redfin Redfin (www.redfin.com) is a technology-powered residential real estate company, including brokerage, iBuying, mortgage, and title services. Founded by software engineers, we run the country’s #1 most-visited brokerage website and offer a host of online tools to consumers, including the Redfin Estimate. We represent people buying and selling homes in over 90 markets in the United States and Canada. In a commission-driven industry, our mission is to redefine real estate in the consumer’s favor. We do this by pairing our own agents with our own technology to create a service that is faster, better, and costs less. Since our launch in 2006, we have helped customers buy or sell more than 235,000 homes worth more than $115 billion.

For more information or to contact a local Redfin real estate agent, visit www.redfin.com. To learn about housing market trends and download data, visit the Redfin Data Center. To be added to Redfin’s press release distribution list, email press@redfin.com. To view Redfin’s press center, click here.