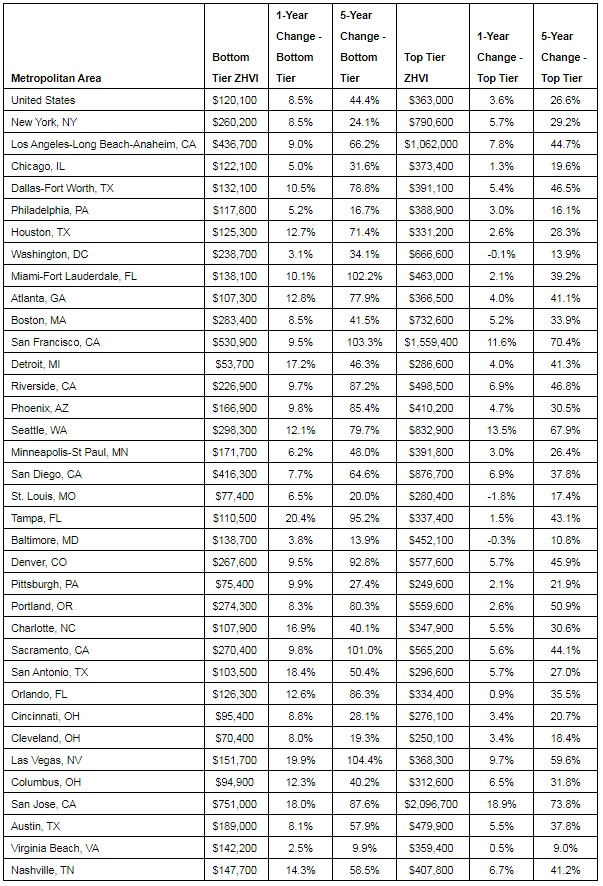

Tax breaks for longtime homeowners are one of many issues analyzed in the annual 50-State Property Tax Comparison Study by the Lincoln Institute of Land Policy and Minnesota Center for Fiscal Excellence

Cambridge, MA – April 17, 2018 (PRNewswire-USNewswire) In Los Angeles, a new owner of a median-valued home pays about $7,000 per year in property taxes – nearly double the $4,000 paid by someone who has owned an identical home for 14 years, the average length of homeownership in the city, according to the annual 50-State Property Tax Comparison Study by the Lincoln Institute of Land Policy and the Minnesota Center for Fiscal Excellence.

![]()

Such preferential treatment of longtime homeowners is a function of California’s Proposition 13, the 1978 ballot initiative that greatly restricts reassessment of property, among its many tax-limiting provisions. Of the ten American cities with the greatest discrepancy in taxes paid by new homeowners and longtime homeowners, six are in California and two are in Florida, where the 1992 Save Our Homes constitutional amendment similarly restricts reassessment.

These discrepancies are just one phenomenon explored through the study’s comprehensive analysis of effective property tax rates – the tax paid as a percentage of market value – in more than 100 cities in every U.S. state and Washington, DC.

As the study makes clear, the property tax is the most stable source of revenue for schools, public safety, and other public services and infrastructure provided by local governments. Effective tax rates vary widely, and, drawing on data for 73 large U.S. cities and a rural municipality in each state, the study explains the reasons why.

As the study makes clear, the property tax is the most stable source of revenue for schools, public safety, and other public services and infrastructure provided by local governments. Effective tax rates vary widely, and, drawing on data for 73 large U.S. cities and a rural municipality in each state, the study explains the reasons why.

Reliance on the property tax is chief among the reasons. Cities with high local sales or income taxes do not need to raise as much revenue from the property tax and thus have lower property tax rates on average. For example, Bridgeport (CT) has one of the highest effective tax rates on the median-valued home, while Birmingham (AL) has one of the lowest. But the average Birmingham resident pays 30 percent more in total local taxes when accounting for sales, income, and other local taxes.

Highest and Lowest Effective Property Tax Rates on a Median-Valued Home (2017)

Property values are the other crucial factor explaining differences in tax rates. Cities with low property values need to impose a much higher tax rate to raise the same revenue as cities with high property values. For example, the effective tax rate on the typical home in Detroit, which has the lowest median home values in the study, is four times higher than in San Francisco, which has the highest. In Detroit, to raise $3,000 per home – the national average tax bill on a median-valued home – would require an effective tax rate 24 times higher than in San Francisco.

The other drivers of variation in property tax rates include the treatment of different classes of property, such as residential and commercial, and the level of local government spending.

The average effective tax rate on a median-valued home was 1.49 percent in 2017, with wide variation across cities. Three cities have effective tax rates that are roughly 2.5 times higher than the average – Bridgeport (CT), Aurora (IL), and Detroit. Conversely, seven cities have tax rates less than half of the study average – Honolulu, Charleston (SC), Boston, Cheyenne (WY), Denver, Birmingham, and Washington, DC.

Commercial property tax rates on office buildings and similar properties also vary significantly across cities. The effective tax rate on a $1 million commercial property is about 2 percent, on average, across the largest cities in each state. The highest rates are in Detroit, New York City, Bridgeport, Chicago, and Providence, where rates are at least 75 percent higher than average. Rates are less than half of the average in Fargo (ND), Virginia Beach, Honolulu, Seattle, and Cheyenne (WY).

Highest and Lowest Effective Property Tax Rates on $1-Million Commercial Property

The study includes a detailed analysis of classification, the practice of taxing specific types of property differently. New York City has the nation’s largest discrepancy between rental apartments and owner-occupied homes, with an effective property tax rate for apartment buildings that is nearly five times higher than the rate for owner-occupied homes, or “homesteads.” Boston has the largest discrepancy between commercial properties and owner-occupied homes, with an effective tax rate on commercial properties that is 4.3 times the rate for homesteads. On average, effective property tax rates for commercial properties are 64 percent higher than for owner-occupied homes, and effective rates for apartments are 33 percent higher.

The report is available for download on the Lincoln Institute website.

The Lincoln Institute of Land Policy seeks to improve quality of life through the effective use, taxation, and stewardship of land. A nonprofit private operating foundation whose origins date to 1946, the Lincoln Institute researches and recommends creative approaches to land as a solution to economic, social, and environmental challenges. Through education, training, publications, and events, we integrate theory and practice to inform public policy decisions worldwide.

The Minnesota Center for Fiscal Excellence was founded in 1926 to promote sound tax policy, efficient spending, and accountable government. As a non-profit, non-partisan group supported by membership dues, the center pursues its mission by educating and informing Minnesotans about sound fiscal policy; providing state and local policy makers with objective, non-partisan research about the impacts of tax and spending policies; and advocating for the adoption of policies reflecting principles of fiscal excellence.