- Early-Stage Delinquencies Drop 0.4 Percentage Points Year Over Year in April

- The Share of Home Loans Transitioning from Current to 30 Days Past Due is the Lowest for the Month of April Since 2000

- Only Hurricane-Impacted States Are Experiencing Significant Serious Delinquency Rate Increases

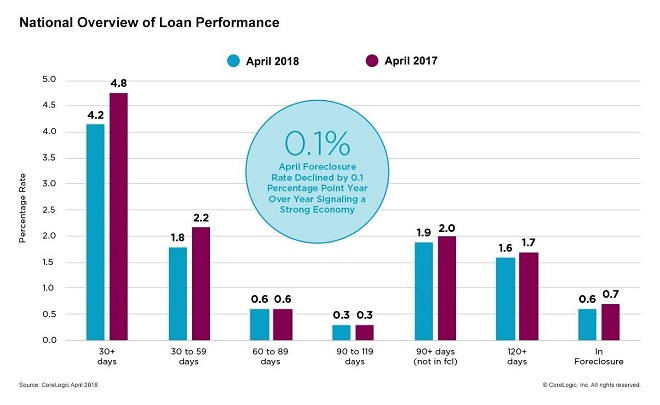

Irvine, CA – July 10, 2018 (BUSINESS WIRE) CoreLogic® (NYSE: CLGX), a leading global property information, analytics and data-enabled solutions provider, today released its monthly Loan Performance Insights Report. The report shows that, nationally, 4.2 percent of mortgages were in some stage of delinquency (30 days or more past due, including those in foreclosure) in April 2018, representing a 0.6 percentage point decline in the overall delinquency rate compared with April 2017, when it was 4.8 percent.

As of April 2018, the foreclosure inventory rate – which measures the share of mortgages in some stage of the foreclosure process – was 0.6 percent, down 0.1 percentage points from 0.7 percent in April 2017. Since August 2017, the foreclosure inventory rate has been steady at 0.6 percent, the lowest level since June 2007, when it was also 0.6 percent. The April 2018 foreclosure inventory rate was the lowest for that month in 11 years; it was also 0.6 percent in April 2007.

Measuring early-stage delinquency rates is important for analyzing the health of the mortgage market. To monitor mortgage performance comprehensively, CoreLogic examines all stages of delinquency, as well as transition rates, which indicate the percentage of mortgages moving from one stage of delinquency to the next.

The rate for early-stage delinquencies – defined as 30 to 59 days past due – was 1.8 percent in April 2018, down from 2.2 in April 2017. The share of mortgages that were 60 to 89 days past due in April 2018 was 0.6 percent, unchanged from April 2017. The serious delinquency rate – defined as 90 days or more past due, including loans in foreclosure – was 1.9 percent in April 2018, down from 2.0 percent in April 2017. The April 2018 serious delinquency rate was the lowest for that month since 2007 when it was 1.6 percent.

“Job growth, home-price appreciation, and full-doc underwriting have pushed delinquency and foreclosure rates to the lowest point in more than a decade,” said Dr. Frank Nothaft, chief economist for CoreLogic. “The latest CoreLogic Home Price Index report revealed the annual national home price growth was 7.1 percent in May, the fastest annual growth in four years. U.S. employers have also continued to employ more individuals, as employment rose by 2.4 million throughout the last 12 months with 213,000 jobs added last month alone. Together, this heightened financial stability is pushing delinquency and foreclosure rates to record lows.”

Since early-stage delinquencies can be volatile, CoreLogic also analyzes transition rates. The share of mortgages that transitioned from current to 30 days past due was 0.8 percent in April 2018, down from 1.2 percent in April 2017. By comparison, in January 2007, just before the start of the financial crisis, the current- to 30-day transition rate was 1.2 percent, while it peaked in November 2008 at 2 percent.

As a result of the 2017 hurricane season, Florida and Texas are the only states showing significant gains in 90-day delinquency rates. According to the CoreLogic Storm Surge Report, Florida has the most densely populated and longest coastal area and thus the most exposure to storm surge flooding (compared to the 19 states analyzed in the report) with more than 2.7 million at-risk homes across five risk categories (Category 1 – Category 5 storms). Louisiana ranks second with more than 817,000 at-risk homes, while Texas ranks third with more than 543,000 at-risk homes. A major storm did not strike Louisiana in 2017, but Florida and Texas are still recovering from Hurricanes Irma and Harvey, respectively.

“Delinquency rates are nearing historic lows, except in areas impacted by extreme weather over the past 18 months, reflecting a long period of strict underwriting practices and improved economic conditions,” said Frank Martell, president and CEO of CoreLogic. “Last year’s hurricanes and wildfires continue to affect today’s default rates. The percent of loans 90 days or more delinquent or in foreclosure are more than double what they were before last autumn’s hurricanes in Houston, Texas and Naples, Florida. The 90-day-plus delinquent or in-foreclosure rate has also quadrupled in Puerto Rico.”

For ongoing housing trends and data, visit the CoreLogic Insights Blog: www.corelogic.com/insights.

Methodology

The data in this report represents foreclosure and delinquency activity reported through April 2018.

The data in this report accounts for only first liens against a property and does not include secondary liens. The delinquency, transition and foreclosure rates are measured only against homes that have an outstanding mortgage. Homes without mortgage liens are not typically subject to foreclosure and are, therefore, excluded from the analysis. Approximately one-third of homes nationally are owned outright and do not have a mortgage. CoreLogic has approximately 85 percent coverage of U.S. foreclosure data.

Source: CoreLogic

The data provided is for use only by the primary recipient or the primary recipient’s publication or broadcast. This data may not be re-sold, republished or licensed to any other source, including publications and sources owned by the primary recipient’s parent company without prior written permission from CoreLogic. Any CoreLogic data used for publication or broadcast, in whole or in part, must be sourced as coming from CoreLogic, a data and analytics company. For use with broadcast or web content, the citation must directly accompany first reference of the data. If the data is illustrated with maps, charts, graphs or other visual elements, the CoreLogic logo must be included on screen or website. For questions, analysis or interpretation of the data, contact Alyson Austin at newsmedia@corelogic.com or Allyse Sanchez at corelogic@ink-co.com. Data provided may not be modified without the prior written permission of CoreLogic. Do not use the data in any unlawful manner. This data is compiled from public records, contributory databases and proprietary analytics, and its accuracy is dependent upon these sources.

About CoreLogic

CoreLogic (NYSE: CLGX) is a leading global property information, analytics and data-enabled solutions provider. The company’s combined data from public, contributory and proprietary sources includes over 4.5 billion records spanning more than 50 years, providing detailed coverage of property, mortgages and other encumbrances, consumer credit, tenancy, location, hazard risk and related performance information. The markets CoreLogic serves include real estate and mortgage finance, insurance, capital markets, and the public sector. CoreLogic delivers value to clients through unique data, analytics, workflow technology, advisory and managed services. Clients rely on CoreLogic to help identify and manage growth opportunities, improve performance and mitigate risk. Headquartered in Irvine, Calif., CoreLogic operates in North America, Western Europe and Asia Pacific. For more information, please visit www.corelogic.com.

CORELOGIC and the CoreLogic logo are trademarks of CoreLogic, Inc. and/or its subsidiaries.

Contacts

CoreLogic

Alyson Austin

Corporate Communications

(949) 214-1414

newsmedia@corelogic.com

or

INK Communications

Allyse Sanchez

(925) 548-2535

corelogic@ink-co.com

Like this:

Like Loading...