Source: car.org

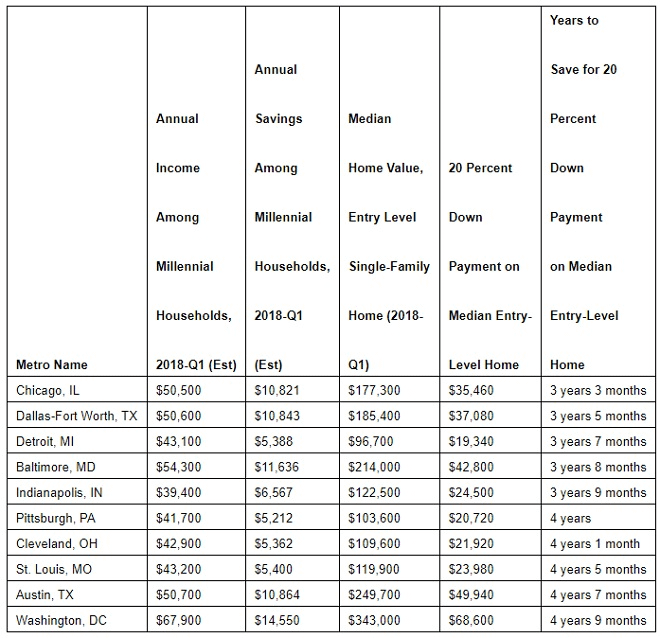

It takes an average of three years to save a 20 percent down payment on a starter home in Chicago, but more than 13 years in Portland, Ore., according to an analysis from RealEstate.com

Seattle, WA – Aug. 20, 2018 (PRNewswire) Saving for a down payment is one of the biggest hurdles to homeownership. However, a new analysis from RealEstate.com, a Zillow Group® brand, identifies 10 metros where first-time buyers may find it easier to save for their future home purchase, and 10 metros where it may be more difficult(i).

![]()

In Chicago, a first-time buyer will need about three years to save a 20 percent down payment on the typical starter home – the fastest of the 35 metros analyzed. First-time buyers in Dallas, Detroit and Baltimore may also find saving for a down payment to take less time than in other metros – with the average millennial household needing just under four years to reach a down payment.

RealEstate.com’s analysis factored in the median household income among millennials (ages 24-36) and their estimated annual household savings to determine how long it would take to save for a 20 percent down payment on starter home — or a home priced within the bottom third of the market.

Since nearly half (44 percent) of buyers move outside of their current city with their home purchase, knowing which metros can help ease some of the down payment burden can be valuable for first-time buyers considering moving(ii).

In Portland, Ore., the estimated annual savings for a millennial household is $5,288 – nearly half of what it is in Chicago ($10,821). Less savings combined with higher home values means a first-time buyer in Portland would need to save for more than 13 years to reach a 20 percent down payment on a starter home – the longest of the metros analyzed. In Denver, San Jose, Calif., and Riverside, Calif., it would take more than 10 years to save a down payment.

While not everyone chooses to put down 20 percent on a home, it is a good goal to aim for, especially for a first-time buyer. According to Zillow Group’s 2017 Consumer Housing Trends Report, 37 percent of first-time buyers (45 percent of all buyers) choose to put 20 percent down or more on their home purchase.

“Contrary to popular belief, millennials want to buy homes, but high home prices, low inventory and stagnant wage growth are some of the many factors that may be driving would-be buyers into delaying homeownership,” says Justin LaJoie, RealEstate.com General Manager. “However, in certain U.S. housing markets first-time buyers can find some relief; they just need to know where to look.”

To help first-time buyers better understand the total cost of homeownership, RealEstate.com allows home shoppers to search based on homes’ “All-In Monthly Price,” which includes estimates for costs such as mortgage, property tax and utilities, giving them a more accurate picture of the cost of homeownership.

Markets where first-time buyers can save for a down payment the fastest:

Markets where it takes first-time buyers longer to save for a down payment:

About Zillow Group

Zillow Group, Inc. (NASDAQ: Z) (NASDAQ: ZG) houses a portfolio of the largest real estate and home-related brands on mobile and the web, which focus on all stages of the home lifecycle: renting, buying, selling and financing. Zillow Group is committed to empowering consumers with unparalleled data, inspiration and knowledge around homes, and connecting them with great real estate professionals. The Zillow Group portfolio of consumer brands includes real estate and rental marketplaces Zillow®, Trulia®, StreetEasy®, HotPads®, Naked Apartments®, RealEstate.com and Out East®. In addition, Zillow Group provides a comprehensive suite of marketing software and technology solutions to help real estate professionals maximize business opportunities and connect with millions of consumers. The Zillow Offers™ marketplace provides homeowners with the opportunity to receive offers from buyers, including Zillow in some metropolitan areas. When Zillow buys a home, it will make necessary updates and list the home for resale on the open market. The company operates a number of business brands for real estate, rental and mortgage professionals, including Mortech®, dotloop®, Bridge Interactive® and New Home Feed®. The company is headquartered in Seattle.

Zillow, Mortech, Bridge Interactive, StreetEasy, HotPads, Out East and New Home Feed are registered trademarks of Zillow, Inc. Zillow Offers is a trademark of Zillow, Inc. Trulia is a registered trademark of Trulia, LLC. dotloop is a registered trademark of DotLoop, LLC. Naked Apartments is a registered trademark of Naked Apartments, LLC.

(i) RealEstate.com estimated the income of employed young adult renters using data from the U.S. Census Bureau’s 2016 American Community Survey, updating incomes through 2018 Q1 using data from the Bureau of Labor Statistics’ Current Employment Statistics. Savings rates for renters were then applied based on data collected as part of the March 2018 Zillow Group Housing Aspirations Report to estimate how much renters save each year. Assuming that a first-time buyer is searching for a home in the bottom third of the home value distribution and puts 20 percent of the home’s value as a down payment, RealEstate.com then calculated how long it would take to save for the down payment.

(ii) According to Zillow Group Consumer Housing Trends Report 2017.

Property taxes, homeowners insurance and common maintenance projects can add up to a surprising annual cost

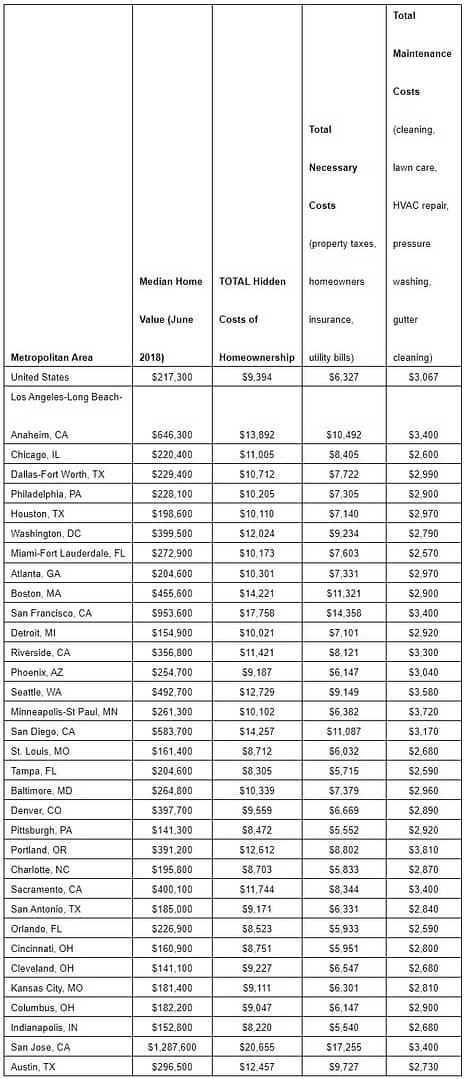

Seattle, WA and San Francisco, CA – Aug. 21, 2018 (PRNewswire) Homeowners can expect to spend about $9,390 every year on costs associated with owning and caring for a home, according to an analysis by Zillow® and Thumbtack.

![]()

When it comes to buying a home, shoppers frequently focus on the sticker price or the monthly mortgage payments, but homeowners are also responsible for additional costs that are often overlooked during the home search, such as property taxes, insurance and maintenance projects.

One-third of buyers say that determining their homebuying budget was a challenge during the home shopping processi. To help understand these additional costs they may face, Zillow and Thumbtack identified several common costs to calculate what homeowners around the country can expect to pay in annual expenses. This analysis also includes utility cost estimates from UtilityScore.

Property taxes, utilities and homeowners insurance are necessary expenses for homeowners. Nationally, these costs add up to $6,327 per year, but can be much higher in more expensive markets. In San Jose, where the typical home is worth $1,287,600, these costs add up to $17,255 per year, the highest of any market analyzed. By contrast, these costs add up to $5,540 annually in Indianapolis, less than one-third of the San Jose total.

Many homeowners also opt to hire professionals for a variety of common home-maintenance projects, including house cleaning, lawn care, carpet cleaning, central air and heating system repairs, gutter cleaning and pressure washing. The nationwide average cost of these tasks is $3,067 per year. Labor costs vary in different parts of the country, so these jobs can be much more expensive depending on where someone lives. In Portland, Oregon, homeowners can expect to pay $3,810 per year for these projects, compared with the $2,570 owners in Miami can expect to spend.

“Ongoing maintenance costs and annual fees are some of the most common surprises for first-time home buyers after they finally become homeowners. While they are shopping, buyers tend to focus on their monthly mortgage payments, but other needs quickly add up after move-in,” said Zillow Senior Economist Aaron Terrazas. “The list price is just the beginning of understanding the costs that come with being a homeowner, and it’s important to understand what other expenses you may have to account for when determining what you can afford.”

“Many basic maintenance costs are often overlooked when calculating the cost of buying a home,” said Lucas Puente, Lead Economist at Thumbtack. “It’s imperative that those looking to buy a home do their homework to avoid any surprising charges.”

Zillow

Zillow is the leading real estate and rental marketplace dedicated to empowering consumers with data, inspiration and knowledge around the place they call home, and connecting them with great real estate professionals. In addition, Zillow operates an industry-leading economics and analytics bureau led by Zillow Group’s Chief Economist Dr. Svenja Gudell. Dr. Gudell and her team of economists and data analysts produce extensive housing data and research covering more than 450 markets at Zillow Real Estate Research. Zillow also sponsors the quarterly Zillow Home Price Expectations Survey, which asks more than 100 leading economists, real estate experts and investment and market strategists to predict the path of the Zillow Home Value Index over the next five years. Launched in 2006, Zillow is owned and operated by Zillow Group, Inc. (NASDAQ: Z and ZG), and headquartered in Seattle.

Zillow is a registered trademark of Zillow, Inc.

Thumbtack

Powering the businesses of hundreds of thousands of local professionals, Thumbtack is one of the largest local services companies in the U.S., offering nearly 1,000 categories, with a working professional in every county in the U.S. Thumbtack has helped customers complete millions of jobs — from plumbing, to catering, to personal training, to math tutoring. Founded in 2008, Thumbtack is headquartered in San Francisco. For more information, please visit: www.thumbtack.com.

(i) https://www.zillow.com/report/2017/buyers/challenges/