Median Home Prices Above Pre-Recession Levels in 65 Percent of Local Markets; Average Homeownership Tenure Increases to New Record High; Distressed Sales Share Drops to 11-Year Low

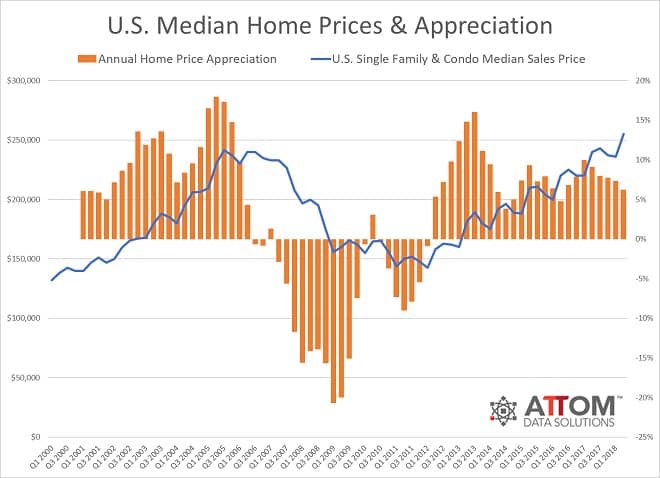

Irvine, CA – July 26, 2018 (PRNewswire) ATTOM Data Solutions, curator of the nation’s premier property database, today released its Q2 2018 U.S. Home Sales Report, which shows that U.S. single family homes and condos sold for a median price of $255,000 in the second quarter, up 6.3 percent from a year ago to a new all-time high but the slowest annual appreciation since Q2 2016.

![]()

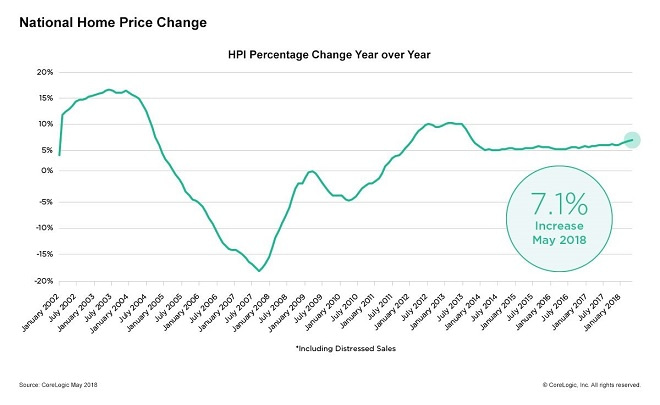

“Annual home price appreciation nationwide has now slowed for five consecutive quarters following a post-election spike to double-digit appreciation in the first quarter of 2017,” said Daren Blomquist, senior vice president at ATTOM Data Solutions. “Although home sellers are still in the driver’s seat of this housing market, moderating home price appreciation is good news for prospective homebuyers and signals that rising mortgage rates and other housing headwinds are cooling red-hot home price appreciation in some areas.”

Annual home price appreciation slows in 66 percent of local markets

Annual home price appreciation in Q2 2018 decelerated from the previous quarter in 80 of the 122 metros (66 percent) analyzed for median home prices, including Los Angeles, Chicago, Dallas-Fort Worth, Houston and Philadelphia.

Counter to the national trend, annual home price appreciation accelerated from the previous quarter in 42 of the 122 metros analyzed (34 percent), including New York, Washington, D.C., Boston, San Francisco and Detroit.

Price-per-square foot appreciation accelerates for homes selling above $1 million

The median price per square foot for homes that sold for $1 million or more in the second quarter increased 5.4 percent from a year ago, accelerating from 3.2 percent annual appreciation in the previous quarter and from 3.4 percent annual appreciation in Q2 2017.

The median price per square foot for homes that sold for under $1 million in the first quarter increased 6.5 percent from a year ago, but that was down from 8.2 percent annual appreciation in the previous quarter and down from 9.0 percent annual appreciation in Q2 2017.

In 49 counties with at least 100 single family and condo sales above $1 million in Q2 2018, median price per square foot appreciation accelerated compared to a year ago in the above-$1 million category in 32 of those counties (65 percent), including Santa Clara County (San Jose), California; Orange County, California; King County (Seattle), Washington; Alameda County (San Francisco), California; and San Diego County, California.

Median price per square foot appreciation decelerated compared to a year ago in the above-$1 million category in 17 of the 49 counties (35 percent) with at least 100 single family home and condo sales above $1 million in Q2 2018, including Los Angeles County, California; Miami-Dade County, Florida; Marin County (San Francisco area), California; Maricopa County (Phoenix), Arizona; and New York County (Manhattan), New York.

Fastest home price appreciation in San Jose, Flint, Seattle, Boise, San Francisco

Among 122 metropolitan statistical areas analyzed in the report, those with the biggest year-over-year increase in median prices were San Jose, California (up 25.0 percent); Flint, Michigan (up 23.7 percent); Seattle, Washington (up 14.3 percent); Boise, Idaho (up 14.3 percent); and San Francisco, California (up 14.2 percent).

“Home prices in the greater Seattle region continue to grow at well above long-term averages for several reasons,” said Matthew Gardner, chief economist with Windermere Real Estate, covering the Seattle market. “Firstly, the area’s booming economy continues to add jobs, driving up demand for housing. Compounding this demand is a lack of new construction housing, which puts substantial upward pressure on home prices in the resale market. Housing affordability is unquestionably a major issue in Seattle; however, ironically enough, the many California buyers relocating to the Seattle area actually think our home prices are a bargain!”

Q2 2018 Home Price Appreciation Heat Map

Median home prices above pre-recession levels in 65 percent of markets

The U.S. median home price of $255,000 in Q2 2018 was 6 percent above the pre-recession peak of $241,648 in Q3 2005.

Median home prices in 79 of the 122 metro areas analyzed for median home prices in the report (65 percent) were above their pre-recession peaks in Q2 2018, led by Houston, Texas (79 percent above); Dallas-Fort Worth (78 percent above); Greeley, Colorado (76 percent above); Denver, Colorado (75 percent above); and San Antonio, Texas (68 percent above).

Median home prices in Q2 2018 were still below pre-recession peaks in 43 of the 122 metros analyzed for median home prices (35 percent), led by Atlantic City, New Jersey (36 percent below); York, Pennsylvania (34 percent below); Salisbury, Maryland (21 percent below); Naples, Florida (19 percent below); and Trenton, New Jersey (18 percent below).

Average homeownership tenure increases to new all-time high of 8.09 years

Homeowners who sold in Q2 2018 had owned their homes for an average of 8.09 years, up from an average homeownership tenure of 7.91 years in Q1 2018 and up from an average homeownership tenure of 7.83 years in Q2 2017.

Counter to the national trend, average homeownership tenure declined in 22 of 108 (20 percent) metropolitan statistical areas analyzed for homeownership tenure, including Sacramento, California; Nashville, Tennessee; Salt Lake City, Utah; Honolulu, Hawaii; and New Haven, Connecticut.

Average home seller gains increase to highest level since Q3 2007

Homeowners who sold in Q2 2018 sold for an average of $58,000 more than their original purchase price, the highest average home seller price gain since Q3 2007.

The $58,000 average home seller price gain in Q2 2018 represented an average 30.2 percent return on the original purchase price, up from an average 28.9 percent return in the first quarter but down from a recent peak of 30.8 percent in Q4 2017.

Among 147 metropolitan statistical areas analyzed for average home seller gains, those with the highest average percentage gain were San Jose, California (116.6 percent); San Francisco, California (85.0 percent); Seattle, Washington (76.5 percent); Boston, Massachusetts (64.3 percent); and Portland, Oregon (62.1 percent).

Distressed sales drop to an 11-year low

Distressed sales — sales of bank-owned homes, short sales, and sales to third-party investors at foreclosure auction — accounted for 11.9 percent of all single family home and condo sales in Q2 2018, down from 14.9 percent in the previous quarter and down from 13.5 percent in Q2 2017 to the lowest level since Q2 2007, an 11-year low.

States with the highest share of distressed sales in Q2 2018 were New Jersey (23.9 percent), Delaware (22.5 percent), Rhode Island (18.6 percent), Connecticut (17.6 percent), and Illinois (17.3 percent).

Among 148 metropolitan statistical areas analyzed for distressed sales, those with the highest share in Q2 2018 were Atlantic City, New Jersey (42.1 percent); Trenton, New Jersey (26.0 percent); Youngstown, Ohio (25.4 percent); Syracuse, New York (24.8 percent); and Hagerstown, Maryland (22.1 percent).

Among 52 metro areas with a population of 1 million or more, those with the highest share of distressed sales in Q2 2018 were Baltimore, Maryland (20.7 percent); Philadelphia, Pennsylvania (20.2 percent); New York-Newark-Jersey City (20.0 percent); Cleveland, Ohio (19.0 percent); and Providence, Rhode Island (18.7 percent).

Other report findings

- Sales to buyers using FHA loans — typically first-time homebuyers — accounted for 10.7 percent of all sales of single family homes and condos in Q2 2018, down from 11.9 percent in the previous quarter and down from 14.0 percent in Q2 2017 to the lowest level since Q1 2008 — a more than 10-year low.

- All-cash purchases accounted for 27.2 percent of all single family home and condo sales in Q2 2018, down from 28.8 percent in the previous quarter and down from 27.6 percent in Q2 2017 to the lowest level since Q3 2016.

- Sales to institutional investors (entities buying at least 10 properties in a calendar year) accounted for 2.0 percent of all single family home and condo sales in Q2 2018, up from 1.9 percent in the previous quarter but still down from 2.3 percent in Q2 2017.

Report methodology

The ATTOM Data Solutions U.S. Home Sales Report provides percentages of distressed sales and all sales that are sold to investors, institutional investors and cash buyers, at the state and metropolitan statistical area. Data is also available at the county and zip code level upon request. The data is derived from recorded sales deeds, foreclosure filings and loan data. Statistics for previous quarters are revised when each new report is issued as more deed data becomes available for those previous months. Median sales prices are calculated based on the sales price on the publicly recorded sales deed when available. If no sales price is recorded then the purchase loan amount is used to calculate median price, and if no purchase loan amount is available, the property’s Automated Valuation Model (AVM) at time of sale is used to calculate the median price.

Definitions

All-cash purchases: sales where no loan is recorded at the time of sale and where ATTOM has coverage of loan data.

Institutional investor purchases: residential property sales to non-lending entities that purchased at least 10 properties in a calendar year.

REO sale: a sale of a property that occurs while the property is actively bank owned (REO).

Third-party foreclosure auction sale: a sale of a property that occurs at the public foreclosure auction (trustee’s sale or sheriff’s sale) in which the property is sold to a third-party buyer and does not transfer back to the foreclosing bank.

Short sale: a sale of a property where the sale price is less than (short) the combined amount of loans secured by the property.

About ATTOM Data Solutions

ATTOM Data Solutions provides premium property data to power products that improve transparency, innovation, efficiency and disruption in a data-driven economy. ATTOM multi-sources property tax, deed, mortgage, foreclosure, environmental risk, natural hazard, and neighborhood data for more than 155 million U.S. residential and commercial properties covering 99 percent of the nation’s population. A rigorous data management process involving more than 20 steps validates, standardizes and enhances the data collected by ATTOM, assigning each property record with a persistent, unique ID — the ATTOM ID. The 9TB ATTOM Data Warehouse fuels innovation in many industries including mortgage, real estate, insurance, marketing, government and more through flexible data delivery solutions that include bulk file licenses, APIs, market trends, marketing lists, match & append and more.

Media Contact:

Christine Stricker

(949) 748-8428

christine.stricker@attomdata.com

Data and Report Licensing:

(949) 502-8313

datareports@attomdata.com