Orlando, FL – Jan. 20, 2023 (PRNewswire) As 2022 ended, Florida’s housing market looked similar to the more traditional market years prior to the pandemic in terms of total closed sales, though it fell short in the year-to-year compared to the unusually strong 2021 sales. The statewide inventory of for-sale existing homes and condo properties showed gains while statewide median sales prices continued to rise year-over-year, despite headwinds from inflation and higher interest rates, according to the latest housing data released by Florida Realtors®.

Year End 2022

Florida Realtors® Chief Economist Dr. Brad O’Connor pointed out that in 2021, Florida’s housing market was “on a sugar high. Overall, closed sales in 2022 were pretty good when you look at the more ‘traditional’ housing market years of 2018 and 2019.”

At the end of 2022, statewide closed sales of existing single-family homes totaled 287,352, down 18% compared to the 2021 year-end level, according to data from Florida Realtors’ research department in partnership with local Realtor boards/associations. Closed sales may occur from 30- to 90-plus days after sales contracts are written.

The statewide median sales price for single-family existing homes at year’s end was $402,500, up 15.7% from the previous year. The median is the midpoint; half the homes sold for more, half for less.

Looking at Florida’s year-to-year comparison for sales of condo-townhouses, a total of 125,494 units sold statewide in 2022, down 21.7% compared to 2021. The statewide median price for condo-townhouse properties at the end of the year was $306,500, up 21.6% from the previous year.

Statewide, the median percentage of the original listing price received by sellers at the end of 2022 continued at about the same level year-over-year in both property type categories at 100% for single-family existing homes and at 99.9% for condo and townhouse units.

According to Florida Realtors’ data, at the end of 2022, in December 2022 and also in 4Q 2022, inventory (active listings) for single-family homes stood at a 2.7-months’ supply, while inventory for condo-townhouse properties was at a 2.8-months’ supply.

“The good news is, we have a lot more inventory than what we had over the pandemic years,” O’Connor said. “Active listings of single-family existing homes more than doubled from a 1-month supply at the end of 2021 to a 2.7-months’ supply at the end of 2022. If we get a little relief in mortgage rates, then all the other factors are still there that make Florida appealing and a strong draw for buyer demand.”

December 2022

In December, closed sales of single-family homes statewide totaled 19,158, down 36.1% from December 2021, while existing condo-townhouse sales totaled 7,677, down 40% year-over-year, according to Florida Realtors’ data.

The statewide median sales prices for both existing single-family homes and condo-townhouse properties rose year-over-year in December 2022. The statewide median sales price for single-family existing homes was $395,000, up 5.6% from the previous year. Meanwhile, the statewide median price for condo-townhouse units was $310,000, up 8.8% over the year-ago figure.

4Q 2022

Statewide closed sales of existing single-family homes totaled 57,004 in the fourth quarter of 2022, down 33.1% compared to the previous-year figure, according to Florida Realtors’ data. The statewide median sales price for existing single-family homes for 4Q 2022 was $400,000, up 9.6% from 4Q 2021.

Looking at Florida’s year-to-year comparison for sales of condo-townhouses in 4Q 2022, a total of 23,117 units sold statewide, down 35.5% from the same quarter in 2021. The statewide median price for condo-townhouse properties for the quarter was $310,000, up 14% over the previous year.

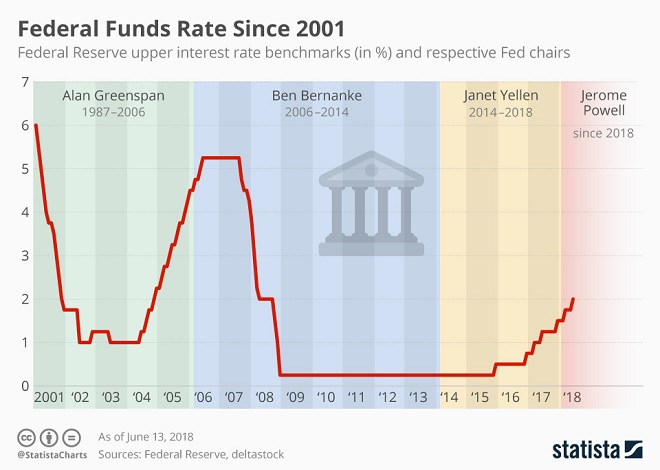

Looking ahead in 2023, Chief Economist O’Connor said mortgage rates – and the Federal Reserve’s action on interest rates as it continues to fight inflation – will influence ongoing market conditions.

He said, “Over the next six months, if mortgage rates don’t rise and return to 7%, that would help encourage buyers – and I think we’ll see mortgage rates stay just above 6% for a while. If we keep seeing more good news on the economic front, then I think we’ll see the housing market respond. Buyer demand is there, perhaps waiting on easing home prices, more supply and other factors.”

To see the full statewide housing activity reports, go to the Florida Realtors’ Newsroom and look under Latest Releases or download the December, 4Q or Year End 2022 data report PDFs under Market Data on the site.

Florida Realtors® serves as the voice for real estate in Florida. It provides programs, services, continuing education, research and legislative representation to more than 238,000 members in 51 boards/associations. Florida Realtors® Newsroom website is available at http://floridarealtors.org/newsroom.

SOURCE Florida Realtors