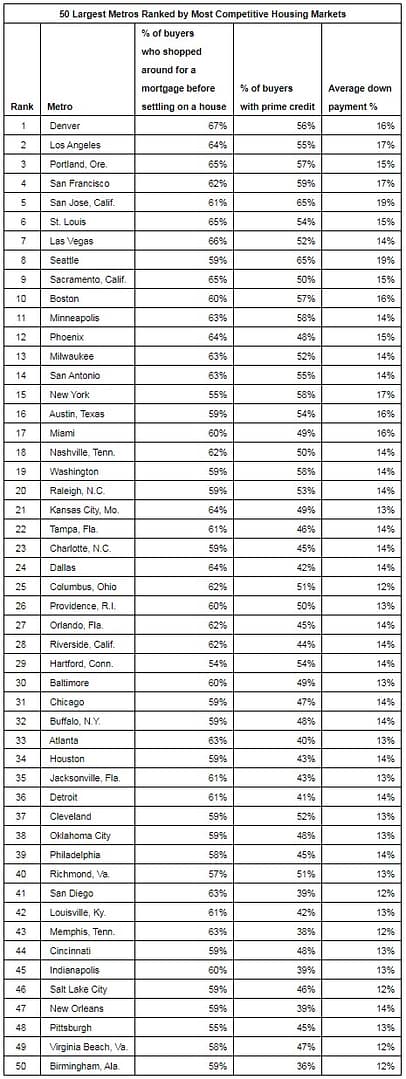

Study ranks 50 largest metros by most competitive housing markets

Charlotte, NC – Jan. 15, 2019 (PRNewswire) LendingTree®, the nation’s leading online loan marketplace, today released its study on which cities have the most competitive housing markets.

![]()

LendingTree ranked the 50 largest metropolitan areas in the United States based on an average of the city’s rank in three categories that contribute to the competitiveness of homebuyers in an area:

- Share of buyers shopping for a mortgage before identifying the house they want

- Average down payment percentage

- Percentage of buyers who have good or excellent credit (above 680)

These criteria were chosen because the average American cannot afford to pay cash for a home — this means that most Americans need good credit to secure a loan, and enough cash to be able to make a substantial down payment. A more competitive buyer has higher credit and the ability to put down larger down payments.

Key Findings:

- Denver, Los Angeles, and Portland, Ore., have the most competitive buyers in the country. Buyers in these areas have higher than average credit and the ability to put down a larger down payment.

- Birmingham, Ala., Virginia Beach, Va., and Pittsburgh have the least competitive buyers in the country. Living in a less competitive market can be beneficial for buyers as it means that the path to homeownership is less challenging than it is in other parts of the country. For example, in these three areas, only 43 percent of mortgage shoppers had prime credit, compared to an average of 49 percent across the 50 largest metros in the U.S.

- The most competitive buyers live out west. Of the top 10 most competitive cities, only two, St. Louis and Boston, were not in a western U.S. state. High-paying tech jobs, common in places like Oregon, San Francisco and Seattle, likely help fuel market competitiveness in some western cities.

- The average down payment percent in the top 10 most competitive metros is 16 percent, two points higher than the average down payment percent found across all the cities looked at in this study. As the housing market cools, this number may fall somewhat, as sellers and lenders accommodate more potential buyers.

- Sixty-three percent of buyers in the 10 most competitive metros shopped around for a mortgage before settling on a house. Shopping around for a mortgage can not only help buyers save money — it can also help them become pre-approved for a mortgage, which makes it easier to purchase a home.

- Fifty-seven percent of buyers in the 10 most competitive metros have good or excellent credit. Across the 50 largest metros in the country, that number is only 49 percent. People who live in more competitive areas should make sure that they carefully monitor and maintain their credit scores.

Metropolitan areas with the most competitive buyers in the U.S.:

Denver

Share of buyers who shopped around for a mortgage before settling on a house: 67%

Share of buyers with good or excellent credit: 56%

Average down payment: 16%

Los Angeles

Share of buyers who shopped around for a mortgage before settling on a house: 64%

Share of buyers with good or excellent credit: 55%

Average down payment: 17%

Portland, OR

Share of buyers who shopped around for a mortgage before settling on a house: 65%

Share of buyers with good or excellent credit: 57%

Average down payment: 15%

“The spring housing market should see more homes on the market than last year, but inventory is still less abundant than historical norms,” said Tendayi Kapfidze, Chief Economist at LendingTree. “Potential buyers should put themselves in the best position by getting a pre-approval ahead of searching for a home. Shopping around for the best mortgage rate will also help buyers maximize their buying power and allow them to compete. Though home price momentum has slowed, prices are still rising and getting a lower rate can help offset the higher prices.”

To view the full report, visit www.lendingtree.com.

About LendingTree

LendingTree (NASDAQ: TREE) is the nation’s leading online marketplace that connects consumers with the choices they need to be confident in their financial decisions. LendingTree empowers consumers to shop for financial services the same way they would shop for airline tickets or hotel stays, comparing multiple offers from a nationwide network of over 500 partners in one simple search, and can choose the option that best fits their financial needs. Services include mortgage loans, mortgage refinances, auto loans, personal loans, business loans, student refinances, credit cards and more. Through the My LendingTree platform, consumers receive free credit scores, credit monitoring and recommendations to improve credit health. My LendingTree proactively compares consumers’ credit accounts against offers on our network, and notifies consumers when there is an opportunity to save money. In short, LendingTree’s purpose is to help simplify financial decisions for life’s meaningful moments through choice, education and support. LendingTree, LLC is a subsidiary of LendingTree, Inc. For more information, go to www.lendingtree.com, dial 800-555-TREE, like our Facebook page and/or follow us on Twitter @LendingTree.

Media Contact: